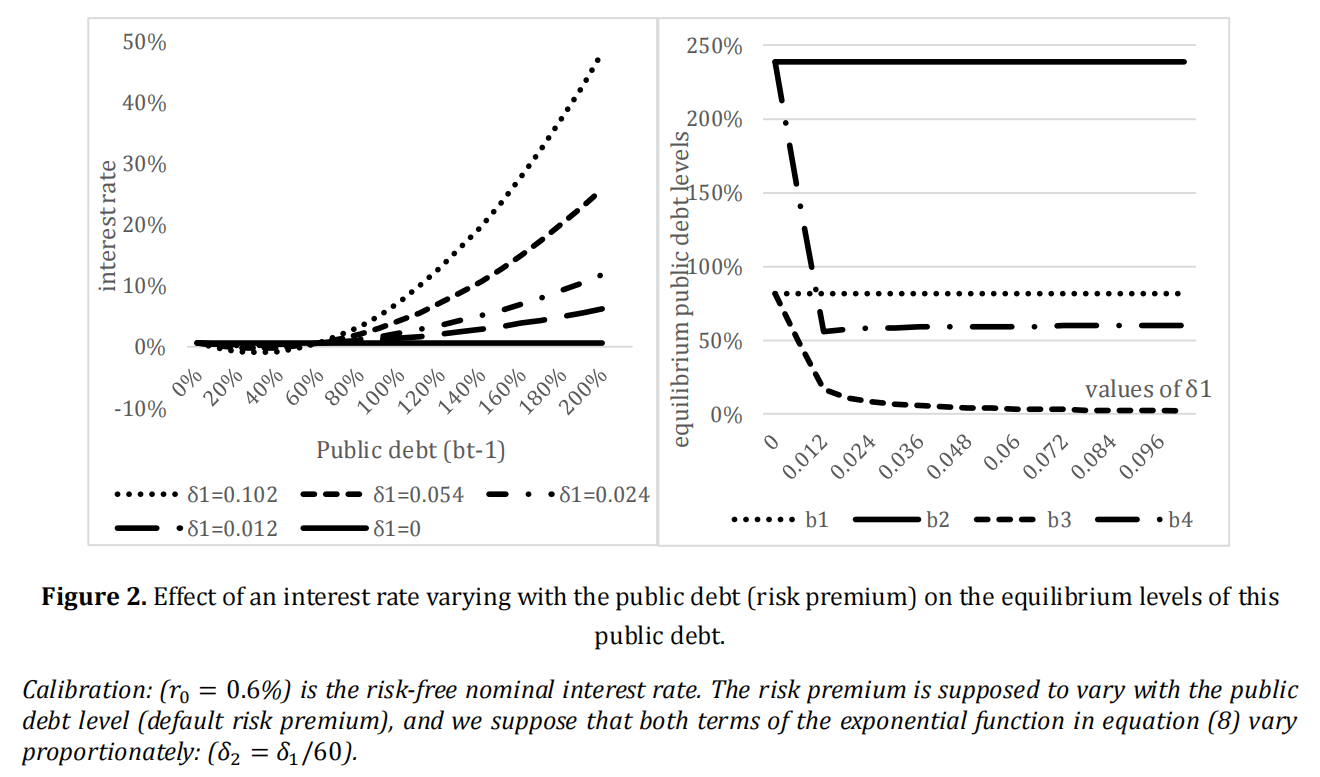

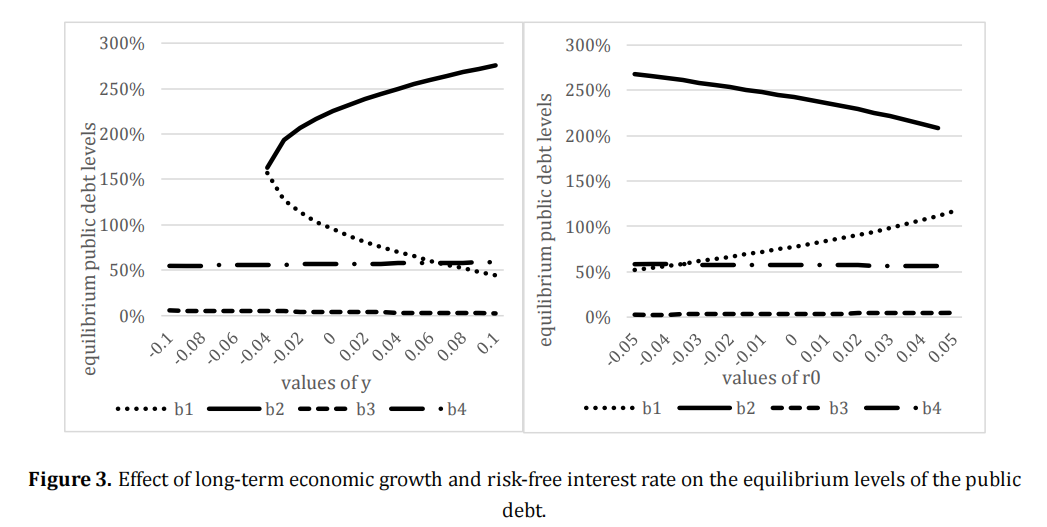

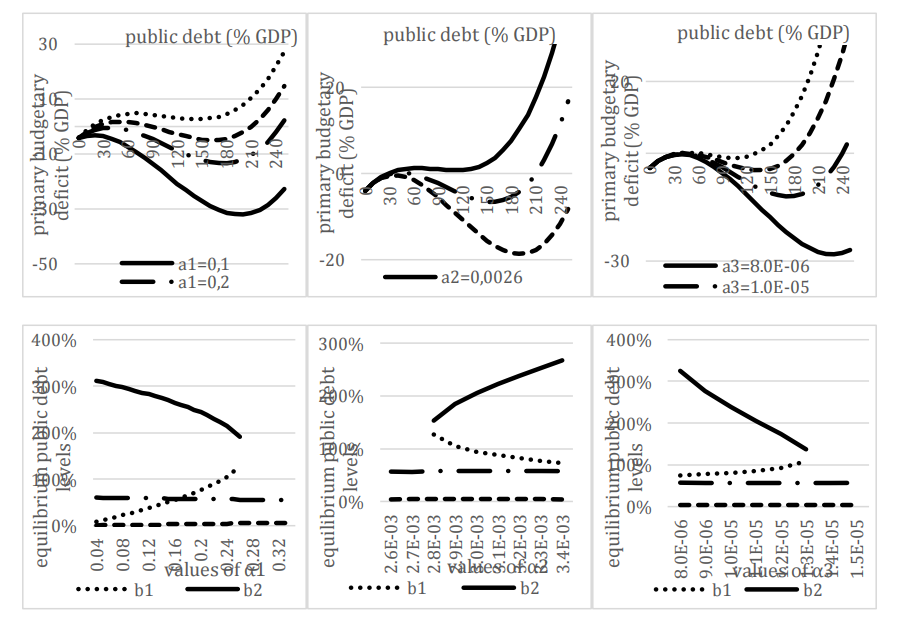

Traditionally, conditions of sustainability of the public debt have long been related quite exclusively to fiscal policy and to budgetary parameters. However, the interaction between fiscal and monetary policies regarding the fixation of the interest rate is fundamental. Indeed, a simple analytical modelling shows that if the nominal interest rate increases exponentially with the public debt, because of a default (credit) risk premium, if the confidence of investors is fundamental, conditions of sustainability of the public debt could be much more difficult to comply with. Indeed, if the interest rate is risk-free, values for which the public debt can be sustainable are less constraining if the long-term GDP growth rate is high, or if the long-term risk-free nominal interest rate is small. They are also less constraining if the country decides to turn to a non-negligible primary budget surplus in case of a high public debt. However, if the interest rate exponentially increases with the public debt level, in case of a significant importance of the default (credit) risk premium, these parameters have very limited consequences on sustainable and equilibrium public debt levels. The sustainable public debt that a government should target is then much smaller than in absence of this risk premium.

Menguy, S. (2023). Fundamental character of the risk premium to influence the sustainability of the public debt. Journal of Economic Analysis, 2(1), 21. doi:10.58567/jea02010008

ACS Style

Menguy, S. Fundamental character of the risk premium to influence the sustainability of the public debt. Journal of Economic Analysis, 2023, 2, 21. doi:10.58567/jea02010008

AMA Style

Menguy S. Fundamental character of the risk premium to influence the sustainability of the public debt. Journal of Economic Analysis; 2023, 2(1):21. doi:10.58567/jea02010008

Chicago/Turabian Style

Menguy, Séverine 2023. "Fundamental character of the risk premium to influence the sustainability of the public debt" Journal of Economic Analysis 2, no.1:21. doi:10.58567/jea02010008

Menguy, S. Fundamental character of the risk premium to influence the sustainability of the public debt. Journal of Economic Analysis, 2023, 2, 21. doi:10.58567/jea02010008

AMA Style

Menguy S. Fundamental character of the risk premium to influence the sustainability of the public debt. Journal of Economic Analysis; 2023, 2(1):21. doi:10.58567/jea02010008

Chicago/Turabian Style

Menguy, Séverine 2023. "Fundamental character of the risk premium to influence the sustainability of the public debt" Journal of Economic Analysis 2, no.1:21. doi:10.58567/jea02010008

APA style

Menguy, S. (2023). Fundamental character of the risk premium to influence the sustainability of the public debt. Journal of Economic Analysis, 2(1), 21. doi:10.58567/jea02010008

Article Metrics

Article Access Statistics

References

Afonso, A., Arghyrou, M. G., and Kontonikas, A. (2015). The Determinants of Sovereign Bond Yield Spreads in the EMU. European Central Bank, Working Paper Series, n°1781, April. https://EconPapers.repec.org/RePEc:ecb:ecbwps:20151781

Alcidi, C., and Gros, D. (2019). Public Debt and the Risk Premium: A Dangerous Doom Loop. CEPS Policy Insights, n°2019-06/2, May. https://www.ceps.eu/wp-content/uploads/2019/03/PI2019_06_CADG_Debt-and-risk-premia-the-doom-loop.pdf

Aldama, P., and Creel, J. (2020). Why Fiscal Regimes matter for Fiscal Sustainability. Banque de France, Working paper, WP 769, June. https://www.banque-france.fr/sites/default/files/medias/documents/wp769.pdf

Alesina, A., De Broeck, M., Prati, A., and Tabellini, G. (1992). Default Risk on Government Debt in OECD Countries. Economic Policy, vol.7, n°15, October, 428–463. https://doi.org/10.2307/1344548

Andrés, J., Burriel, P., and Shi, W. (2020). Debt Sustainability and Fiscal Space in a Heterogeneous Monetary Union: Normal Times vs the Zero Lower Bound. Working Paper, n°2001, Banco de España. https://www.bde.es/f/webbde/SES/Secciones/Publicaciones/PublicacionesSeriadas/DocumentosTrabajo/20/Files/dt2001e.pdf

Ardagna, S., Caselli, F., and Lane, T. (2007). Fiscal Discipline and the Cost of Public Debt Service: Some Estimates for OECD Countries. The B.E. Journal of Macroeconomics, vol.7, n°1, August, 1-35. https://www.ecb.europa.eu/pub/pdf/scpwps/ecbwp411.pdf

Baldacci, E., and Kumar, M. S. (2010). Fiscal Deficits, Public Debt, and Sovereign Bond Yields. IMF Working Paper, WP/10/184. https://www.imf.org/external/pubs/ft/wp/2010/wp10184.pdf

Bernoth, K., Von Hagen, J., and Schuknecht, L. (2012). Sovereign Risk Premiums in the European Government Bond Market. Journal of International Money and Finance, vol. 31, n°5, 975-995. https://www.sciencedirect.com/science/article/abs/pii/S0261560611001914

Bi, H. (2012). Sovereign Default Risk Premia, Fiscal Limits, and Fiscal Policy. European Economic Review, vol.56, n°3, 389–410. http://www.sciencedirect.com/science/article/pii/S0014292111001085

Bischi G. I., Giombini, G., and Travaglini, G. (2022). Monetary and Fiscal Policy in a Nonlinear Model of Public Debt. Economic Analysis and Policy, vol.76, December, 397-409. https://www.sciencedirect.com/science/article/abs/pii/S0313592622001382

Bohn, H. (1998). The Behavior of U.S. Public Debt and Deficits. Quarterly Journal of Economics, vol.113, n°3, 949–963. http://hdl.handle.net/10.1162/003355398555793

Checherita-Westphal, C., Hughes-Hallett, A., and Rother, P. (2014). Fiscal Sustainability using Growth-Maximising Debt Targets. Applied Economics, vol.46, n°6, 638–647. https://www.ecb.europa.eu/pub/pdf/scpwps/ecbwp1472.pdf

Checherita-Westphal, C., and Zdarek, V. (2017). Fiscal Reaction Function and Fiscal Fatigue: Evidence for the Euro Area. ECB Working Paper, n°2036, March. https://www.ecb.europa.eu/pub/pdf/scpwps/ecbwp2036.en.pdf

Combes, J.-L., Minea, A., and Sow, M. (2017). Is Fiscal Policy Always Counter-(Pro-) Cyclical? The Role of Public Debt and Fiscal Rules. Economic Modelling, vol.65, issue C, 138–46. https://www.sciencedirect.com/science/article/abs/pii/S0264999316304072

De Grauwe, P., and Ji, Y. (2013). Self-Fulfilling Crises in the Eurozone: An Empirical Test. Journal of International Money and Finance, vol.34, issue C, April, 15-36. https://www.sciencedirect.com/science/article/pii/S0261560612001829

Delatte, A-L, Fouquau, J., and Portes, R. (2017) Regime-Dependent Sovereign Risk Pricing During the Euro Crisis. Review of Finance, vol.21, n°1, 363–385. https://academic.oup.com/rof/article/21/1/363/2670359

Engen, E., and Hubbard, R. G. (2004). Federal Government Debt and Interest Rates. NBER Working Papers 10681, August. http://www.nber.org/chapters/c6669

Escolano, J. (2010). A Practical Guide to Public Debt Dynamics, Fiscal Sustainability, and Cyclical Adjustment of Budgetary Aggregate. Technical Notes and Manuals n°2010/02, International Monetary Fund, January. https://www.imf.org/external/pubs/ft/tnm/2010/tnm1002.pdf

Fournier, J.-M., and Fall, F. (2017). Limits to Government Debt Sustainability in OECD Countries. Economic Modelling, vol.66, issue C, November, 30-41. https://www.sciencedirect.com/science/article/abs/pii/S0264999316308938

Ghosh, A. R., Kim, J. I., Mendoza, E. G., Ostry, J. D., and Qureshi, M. S. (2013). Fiscal Fatigue, Fiscal Space and Debt Sustainability in Advanced Economies. The Economic Journal, vol.123, n°566, February, F4–F30. https://academic.oup.com/ej/article-abstract/123/566/F4/5079491

Juessen, F., Linnemann, L., and Schabert, A. (2016). Default Risk Premia on Government Bonds in a Quantitative Macroeconomic Model. Macroeconomic Dynamics, vol.20, n°1, January, 380-403. https://www.cambridge.org/core/product/identifier/S1365100514000431/type/journal_article

Larch, M., Orseau, E. and Van der Wielen, W. (2021). Do EU Fiscal Rules support or hinder Counter-Cyclical Fiscal Policy? Journal of International Money and Finance, vol.112, issue C, April, 102328. https://www.sciencedirect.com/science/article/abs/pii/S0261560620302849

Laubach, T. (2009). New Evidence on the Interest Rate Effects of Budget Deficits and Debt. Journal of the European Economic Association, vol.7, n°4, June, 858-885. https://www.jstor.org/stable/40282791

Medeiros, J. (2012). Stochastic Debt Simulation using VAR Models and a Panel Fiscal Reaction Function – Results for a Selected Number of Countries. European Economy, Economic Papers, n°459, European Commission, July. https://ec.europa.eu/economy_finance/publications/economic_paper/2012/pdf/ecp459_en.pdf

Ostry, J. D., Ghosh, A. R., Kim, J. I., and Qureshi, M. S. (2010). Fiscal Space. IMF Staff Position Note, SPN/10/11, International Monetary Fund. https://www.imf.org/external/pubs/ft/spn/2010/spn1011.pdf