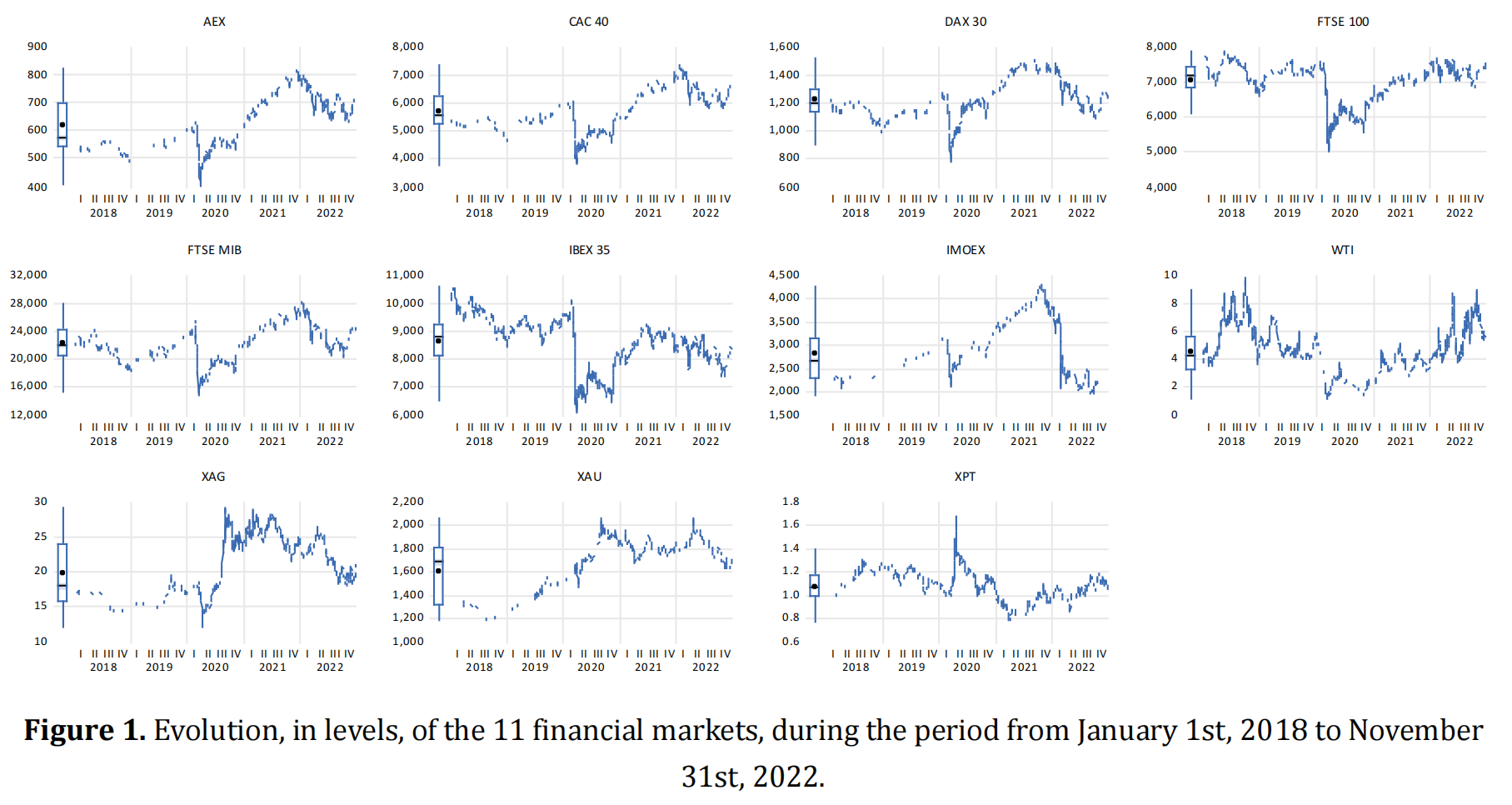

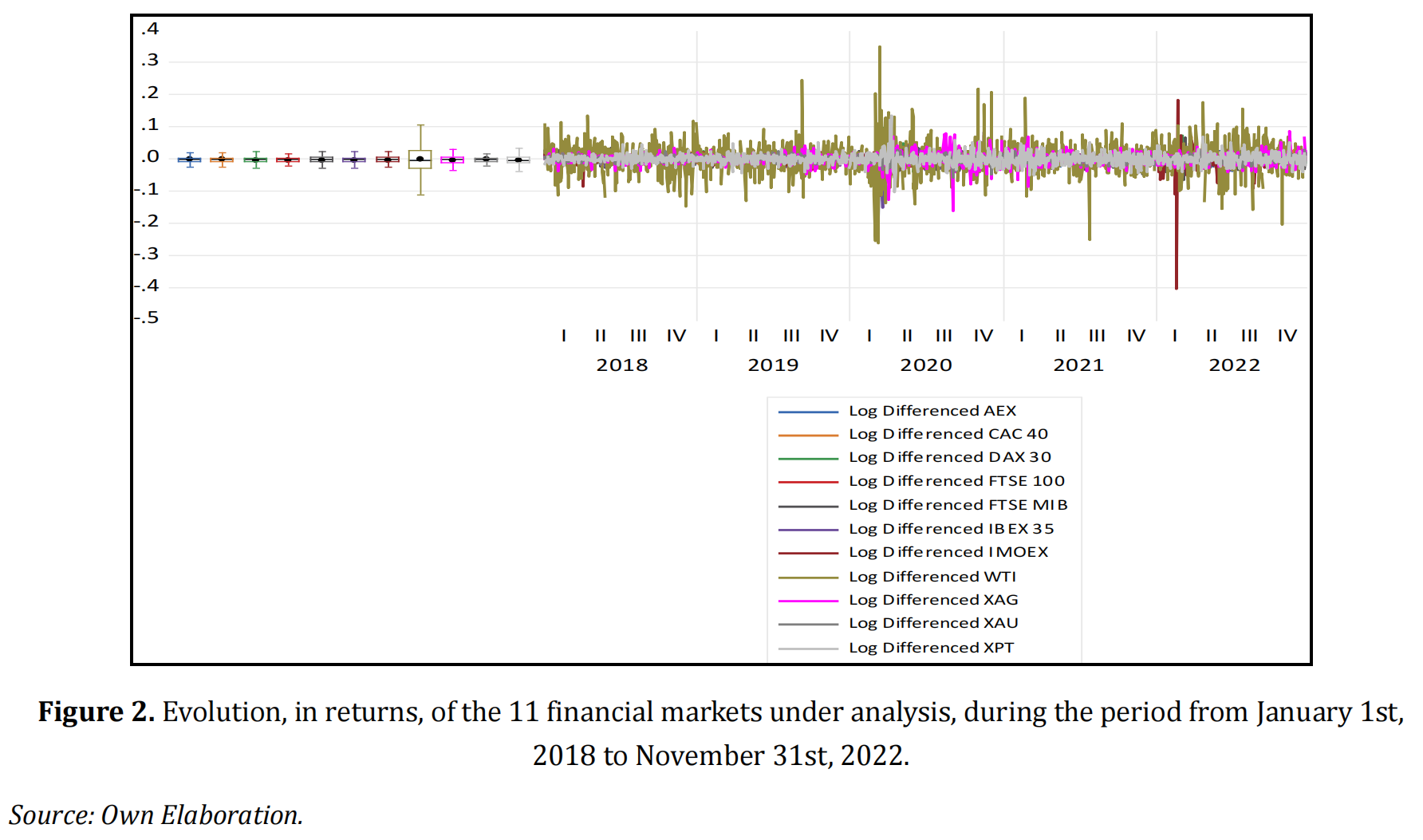

In light of the events of 2020 and 2022, this study aims to examine the co-movements between the capital markets of the Netherlands (AEX), France (CAC 40), Germany (DAX 30), the United Kingdom (FTSE 100), Italy (FTSE MIB), Spain (IBEX 35), Russia (IMOEX), and spot prices of crude oil (WTI), silver (XAG), gold (XAU), and platinum (XPT) from January 1, 2018 to December 31, 2022. The purpose of this analysis is to answer the following research question: (i) Did the events of 2020 and 2022 increase the shocks between stock markets and WTI, XAG, XAU, and XPT prices? The findings indicate that time series do not follow a normal distribution and are stationary. In response to the question of investigation, we found that during the Tranquil period, it was possible to verify the existence of 28 causal relationships (out of 110 possibilities). During the stress period, there was a very significant increase in the number of causal relationships between the market pairs under analysis (62 causal relationships out of 110 possibilities), including a relative increase in the influence of commodities on capital markets and capital markets on commodities. These findings show that during the events of 2020 and 2022, capital markets and commodities significantly accentuated their co-movements among themselves, indicating that alternative markets such as WTI, XAG, XAU, and XPT do not provide safe-haven properties. These results have implications for portfolio diversification during times of global economic uncertainty.

Teixeira Dias, R. M., Horta, N. R., & Chambino, M. (2023). Portfolio rebalancing in times of stress: Capital markets vs. Commodities. Journal of Economic Analysis, 2(1), 18. doi:10.58567/jea02010005

ACS Style

Teixeira Dias, R. M.; Horta, N. R.; Chambino, M. Portfolio rebalancing in times of stress: Capital markets vs. Commodities. Journal of Economic Analysis, 2023, 2, 18. doi:10.58567/jea02010005

AMA Style

Teixeira Dias R. M., Horta N. R., Chambino M.. Portfolio rebalancing in times of stress: Capital markets vs. Commodities. Journal of Economic Analysis; 2023, 2(1):18. doi:10.58567/jea02010005

Chicago/Turabian Style

Teixeira Dias, Rui M.; Horta, Nicole R.; Chambino, Mariana 2023. "Portfolio rebalancing in times of stress: Capital markets vs. Commodities" Journal of Economic Analysis 2, no.1:18. doi:10.58567/jea02010005

Teixeira Dias, R. M.; Horta, N. R.; Chambino, M. Portfolio rebalancing in times of stress: Capital markets vs. Commodities. Journal of Economic Analysis, 2023, 2, 18. doi:10.58567/jea02010005

AMA Style

Teixeira Dias R. M., Horta N. R., Chambino M.. Portfolio rebalancing in times of stress: Capital markets vs. Commodities. Journal of Economic Analysis; 2023, 2(1):18. doi:10.58567/jea02010005

Chicago/Turabian Style

Teixeira Dias, Rui M.; Horta, Nicole R.; Chambino, Mariana 2023. "Portfolio rebalancing in times of stress: Capital markets vs. Commodities" Journal of Economic Analysis 2, no.1:18. doi:10.58567/jea02010005

APA style

Teixeira Dias, R. M., Horta, N. R., & Chambino, M. (2023). Portfolio rebalancing in times of stress: Capital markets vs. Commodities. Journal of Economic Analysis, 2(1), 18. doi:10.58567/jea02010005

Article Metrics

Article Access Statistics

References

Chkili, W. (2022). The links between gold, crude oil prices and Islamic stock markets in a regime switching environment. Eurasian Economic Review, 12(1). https://doi.org/10.1007/s40822-022-00202-y

Cong, R. G., Wei, Y. M., Jiao, J. L., & Fan, Y. (2008). Relationships between crude oil price shocks and stock market: An empirical analysis from China. Energy Policy, 36(9). https://doi.org/10.1016/j.enpol.2008.06.006

Dias, R., & Carvalho, L. C. (2020). Hedges and safe havens: An examination of stocks, gold and silver in Latin America’s stock market. Revista de Administração Da UFSM, 13(5), 1114–1132. https://doi.org/10.5902/1983465961307

Dias, R., da Silva, J. V., & Dionísio, A. (2019). Financial markets of the LAC region: Does the crisis influence the financial integration? International Review of Financial Analysis, 63(January), 160–173. https://doi.org/10.1016/j.irfa.2019.02.008

Dias, R., Pardal, P., Teixeira, N., & Horta, N. (2022). Tail Risk and Return Predictability for Europe ’ s Capital Markets : An Approach in Periods of the. December. https://doi.org/10.4018/978-1-6684-5666-8.ch015

Dias, R., Pardal, P., Teixeira, N., & Machová, V. (2020). Financial Market Integration of ASEAN-5 with China. Littera Scripta, 13(1). https://doi.org/10.36708/littera_scripta2020/1/4

Dias, R., Pereira, J. M., & Carvalho, L. C. (2022). Are African Stock Markets Efficient? A Comparative Analysis Between Six African Markets, the UK, Japan and the USA in the Period of the Pandemic. Naše Gospodarstvo/Our Economy, 68(1), 35–51. https://doi.org/10.2478/ngoe-2022-0004

Dias, R., Santos, H., Heliodoro, P., Vasco, C., & Alexandre, P. (2021). Wti Crude oil Shocks in Eastern European Stock Markets: a Var Approach. 5th EMAN Conference Proceedings (Part of EMAN Conference Collection), October, 71–84. https://doi.org/10.31410/eman.2021.71

Dias, R. T., & Carvalho, L. (2021). The Relationship Between Gold and Stock Markets During the COVID-19 Pandemic. May, 462–475. https://doi.org/10.4018/978-1-7998-6643-5.ch026

Dickey, D., & Fuller, W. (1981). Likelihood ratio statistics for autoregressive time series with a unit root. Econometrica, 49(4), 1057–1072. https://doi.org/10.2307/1912517

El Hedi Arouri, M., Lahiani, A., & Nguyen, D. K. (2015). World gold prices and stock returns in China: Insights for hedging and diversification strategies. Economic Modelling, 44(January 1982), 273–282. https://doi.org/10.1016/j.econmod.2014.10.030

Gharib, C., Mefteh-Wali, S., & Jabeur, S. Ben. (2021). The bubble contagion effect of COVID-19 outbreak: Evidence from crude crude oil and gold markets. Finance Research Letters, 38. https://doi.org/10.1016/j.frl.2020.101703

Gujarati, D. N. (2004). Basic Econometrics. In New York. https://doi.org/10.1126/science.1186874

Horta, N., Dias, R., Revez, C., Heliodoro, P., & Alexandre, P. (2022). Spillover and Quantitative Link Between Cryptocurrency Shocks and Stock Returns: New Evidence From G7 Countries. Balkans Journal of Emerging Trends in Social Sciences, 5(1), 1–14. https://doi.org/10.31410/balkans.jetss.2022.5.1.1-14

Hussain Shahzad, S. J., Bouri, E., Roubaud, D., & Kristoufek, L. (2020). Safe haven, hedge and diversification for G7 stock markets: Gold versus bitcoin. Economic Modelling. https://doi.org/10.1016/j.econmod.2019.07.023

Im, K. S., Pesaran, M. H., & Shin, Y. (2003). Testing for unit roots in heterogeneous panels. Journal of Econometrics. https://doi.org/10.1016/S0304-4076(03)00092-7

Jarque, C. M., & Bera, A. K. (1980). Efficient tests for normality, homoscedasticity and serial independence of regression residuals. Economics Letters, 6(3), 255–259. https://doi.org/10.1016/0165-1765(80)90024-5

Levin, A., Lin, C. F., & Chu, C. S. J. (2002). Unit root tests in panel data: Asymptotic and finite-sample properties. Journal of Econometrics. https://doi.org/10.1016/S0304-4076(01)00098-7

Naeem, M. A., Hasan, M., Arif, M., Balli, F., & Shahzad, S. J. H. (2020). Time and frequency domain quantile coherence of emerging stock markets with gold and crude oil prices. Physica A: Statistical Mechanics and Its Applications. https://doi.org/10.1016/j.physa.2020.124235

Pardal, P., Dias, R., Teixeira, N. & Horta, N. (2022). The Effects of Russia ’ s 2022 Invasion of Ukraine on Global Markets : An Analysis of Particular Capital and Foreign Exchange Markets. https://doi.org/10.4018/978-1-6684-5666-8.ch014

Pardal, P., Dias, R. T., Santos, H., & Vasco, C. (2021). Central European Banking Sector Integration and Shocks During the Global Pandemic (COVID-19). June, 272–288. https://doi.org/10.4018/978-1-7998-6926-9.ch015

Perron, P., & Phillips, P. C. B. (1988). Testing for a Unit Root in a Time Series Regression. Biometrika, 2(75), 335–346. https://doi.org/10.1080/07350015.1992.10509923

Silva, R., Dias, R., Heliodoro, P., & Alexandre, P. (2020). Risk Diversification in Asean-5 Financial Markets: an Empirical Analysis in the Context of the Global Pandemic (Covid-19). 6th LIMEN Selected Papers (Part of LIMEN Conference Collection), 6(July), 15–26. https://doi.org/10.31410/limen.s.p.2020.15

Sun, M., Song, H., & Zhang, C. (2022). The Effects of 2022 Russian Invasion of Ukraine on Global Stock Markets: An Event Study Approach. SSRN Electronic Journal, 262–280. https://doi.org/10.2139/ssrn.4051987

Teixeira, N., Dias, R., & Pardal, P. (2022). The gold market as a safe haven when stock markets exhibit pronounced levels of risk : evidence during the China crisis and the COVID-19 pandemic. April, 27–42.

Teixeira, N., Dias, R., Pardal, P., & Horta, N. (2022). Financial Integration and Comovements Between Capital Markets and Crude oil Markets : An Approach During the Russian. December. https://doi.org/10.4018/978-1-6684-5666-8.ch013

Umar, Z., Trabelsi, N., & Zaremba, A. (2021). Crude oil shocks and equity markets: The case of GCC and BRICS economies. Energy Economics, 96. https://doi.org/10.1016/j.eneco.2021.105155