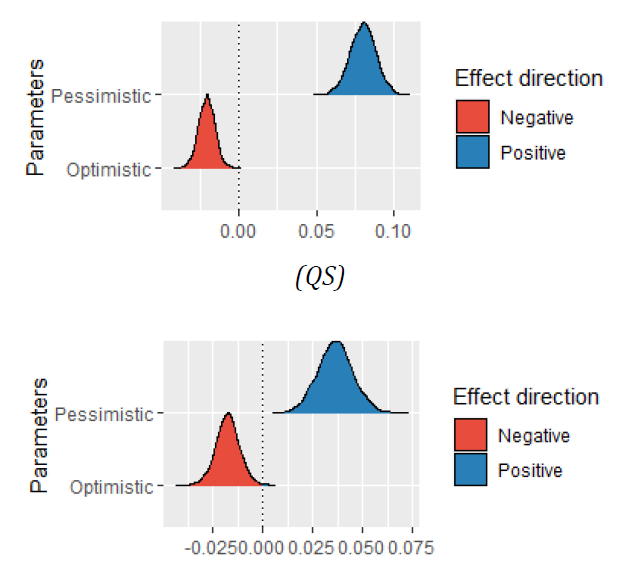

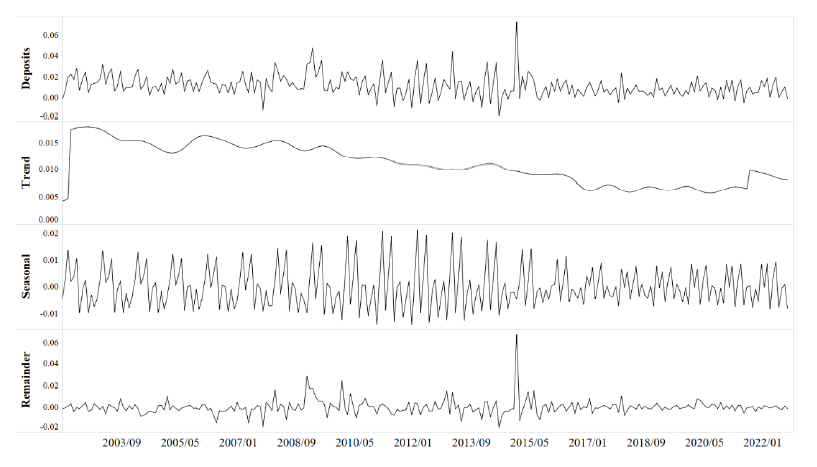

Bank deposit is closely related to systemic risks. In addition, considering that resident deposits in China have significant seasonal characteristics, this paper focuses on which component of deposits drives the systemic risk volatility, that is, it can supplement the existing forecast information. We use X-13ARIMA-SEATS to decompose deposit into three subsequences. The research findings show that the forecast effect of subsequence models is better than that of benchmark series. Most importantly, the model with trend component has the best forecast performance.

Huang, Y.; Soyano, K. Which Component of Deposit Drives Systemic Risk Volatility. Economic Analysis Letters, 2022, 1, 1. https://doi.org/10.58567/eal01010001

AMA Style

Huang Y, Soyano K. Which Component of Deposit Drives Systemic Risk Volatility. Economic Analysis Letters; 2022, 1(1):1. https://doi.org/10.58567/eal01010001

Huang, Y., & Soyano, K. (2022). Which Component of Deposit Drives Systemic Risk Volatility. Economic Analysis Letters, 1(1), 1. https://doi.org/10.58567/eal01010001

Article Metrics

Article Access Statistics

References

Adrian, T., & Boyarchenko, N. (2018). Liquidity policies and systemic risk. Journal of Financial Intermediation, 35, 45-60. https://doi.org/10.1016/j.jfi.2017.08.005

Anginer, D., Demirguc-Kunt, A., & Mare, D. S. (2018). Bank capital, institutional environment and systemic stability. Journal of Financial Stability, 37, 97-106. https://doi.org/10.1016/j.jfs.2018.06.001

Castiglionesi, F., & Eboli, M. (2018). Liquidity Flows in Interbank Networks. Review of Finance, 22(4), 1291-1334. https://doi.org/10.1093/rof/rfy013

Chen, W., Zhang, Z. W., Hamori, S., & Kinkyo, T. (2021). Not all bank systemic risks are alike: Deposit insurance and bank risk revisited. International Review of Financial Analysis, 77, Article 101855. https://doi.org/10.1016/j.irfa.2021.101855

Engle, R. F., Ghysels, E., & Sohn, B. (2013). Stock Market Volatility And Macroeconomic Fundamentals. The Review of Economics and Statistics, 95(3), 776-797. http://www.jstor.org/stable/43554794

Fang, L., Chen, B., Yu, H., & Qian, Y. (2017). The importance of global economic policy uncertainty in predicting gold futures market volatility: A GARCH-MIDAS approach. Journal of Futures Markets, 38. https://doi.org/10.1002/fut.21897

Kanas, A., & Zervopoulos, P. D. (2020). Systemic risk-shifting in US commercial banking. Review of Quantitative Finance and Accounting, 54(2), 517-539. https://doi.org/10.1007/s11156-019-00797-5

Louhichi, W., Saghi, N., Srour, Z., & Viviani, J. L. (2022). The effect of liquidity creation on systemic risk: evidence from European banking sector. Annals of Operations Research. https://doi.org/10.1007/s10479-022-04836-8