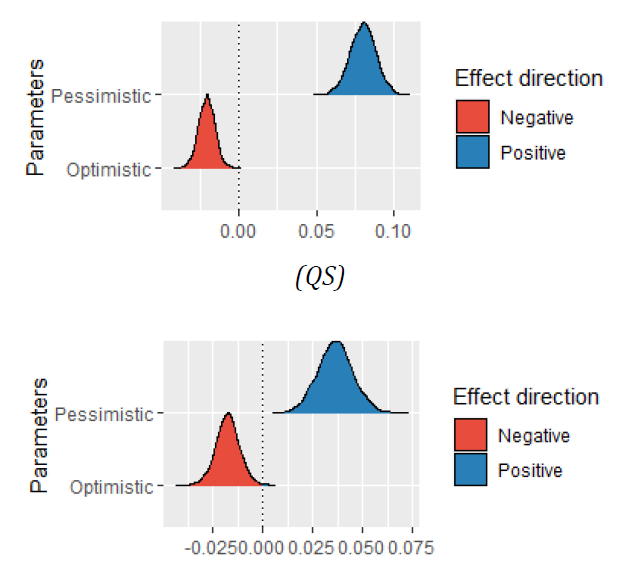

Liquidity can be a real phenomenon for execution of the financial holding. Its risk falls in debate to impose a conditional cost on the counterparty. The time-varying liquidity is often linked to the expected fundamental value of an investment. In this work, the microblogging-based informed transaction is examined as a determinant of the liquidity-facilitating cost. Most importantly, this study investigates the economic blockade era and post-pandemic uncertainty. The sentiment indicators were found to be determinants of liquidity. These findings were consistent in the post-pandemic period. However, the investor pessimistic sentiment was a priced risk factor in liquidity during the economic blockade period. Based on the Bayesian theorem, a relativeness was reported between sentiment indicators and the liquidity-facilitating cost. The same findings were depicted in environments of the pandemic era. Nevertheless, the posterior probability indicated an occurrence of the liquidity-associated cost in response to the pessimistic sentiments during the economic blockade period. This quantification may have potential implications in terms of exploring liquidity from the microblogging perceptive.

Saleemi, J. (2023). Microblogging Perceptive and Pricing Liquidity: Exploring Asymmetric Information as a Risk Determinant of Liquidity in the Pandemic Environments. Economic Analysis Letters, 2(1), 11. doi:10.58567/eal02010001

ACS Style

Saleemi, J. Microblogging Perceptive and Pricing Liquidity: Exploring Asymmetric Information as a Risk Determinant of Liquidity in the Pandemic Environments. Economic Analysis Letters, 2023, 2, 11. doi:10.58567/eal02010001

AMA Style

Saleemi J. Microblogging Perceptive and Pricing Liquidity: Exploring Asymmetric Information as a Risk Determinant of Liquidity in the Pandemic Environments. Economic Analysis Letters; 2023, 2(1):11. doi:10.58567/eal02010001

Chicago/Turabian Style

Saleemi, Jawad 2023. "Microblogging Perceptive and Pricing Liquidity: Exploring Asymmetric Information as a Risk Determinant of Liquidity in the Pandemic Environments" Economic Analysis Letters 2, no.1:11. doi:10.58567/eal02010001

Saleemi, J. Microblogging Perceptive and Pricing Liquidity: Exploring Asymmetric Information as a Risk Determinant of Liquidity in the Pandemic Environments. Economic Analysis Letters, 2023, 2, 11. doi:10.58567/eal02010001

AMA Style

Saleemi J. Microblogging Perceptive and Pricing Liquidity: Exploring Asymmetric Information as a Risk Determinant of Liquidity in the Pandemic Environments. Economic Analysis Letters; 2023, 2(1):11. doi:10.58567/eal02010001

Chicago/Turabian Style

Saleemi, Jawad 2023. "Microblogging Perceptive and Pricing Liquidity: Exploring Asymmetric Information as a Risk Determinant of Liquidity in the Pandemic Environments" Economic Analysis Letters 2, no.1:11. doi:10.58567/eal02010001

APA style

Saleemi, J. (2023). Microblogging Perceptive and Pricing Liquidity: Exploring Asymmetric Information as a Risk Determinant of Liquidity in the Pandemic Environments. Economic Analysis Letters, 2(1), 11. doi:10.58567/eal02010001

Article Metrics

Article Access Statistics

References

Acharya, V. V., & Pedersen, L. H. (2005). Asset pricing with liquidity risk. Journal of Financial Economics, 77(2), 375-410. https://doi.org/10.1016/j.jfineco.2004.06.007

Ahundjanov, B. B., Akhundjanov, S. B., & Okhunjanov, B. B. (2021). Risk perception and oil and gasoline markets under COVID-19. Journal of Economics and Business, 115, 105979. https://doi.org/10.1016/j.jeconbus.2020.105979.

Amihud, Y., & Mendelson, H. (2008). Liquidity, the value of the firm, and corporate finance. Journal of Applied Corporate Finance, 20(2), 32–45. https://doi.org/10.1111/j.1745-6622.2008.00179.x

Bank, S., Yazar, E. E., & Sivri, U. (2019). Can social media marketing lead to abnormal portfolio returns? European Research on Management and Business Economics, 25, 54-62. https://doi.org/10.1016/j.iedeen.2019.04.006

Bartov, E., Faurel, L., & Mohanram, P. (2018). Can Twitter help predict firm-level earnings and stock returns? The Accounting Review, 93(3), 25-27. https://doi.org/10.2308/accr-51865

Conlon, A., & McGee, R. (2020). Safe haven or risky hazard? Bitcoin during the Covid-19 bear market. Finance Research Letters, 35, 101607. https://doi.org/10.1016/j.frl.2020.101607

Corwin, S. A., & Schultz, P. (2012). A Simple Way to Estimate Bid-Ask Spreads from Daily High and Low Prices. The Journal of Finance, 67(2), 719-760. https://doi.org/10.1111/j.1540-6261.2012.01729.x

David, S., Inácio Jr, C., & Machado, J. (2021). The recovery of global stock markets indices after impacts due to pandemics. Research in International Business and Finance, 55, 101335. https://doi.org/10.1016/j.ribaf.2020.101335.

Fong, K. Y., Holden, C. W., & Trzcinka, C. A. (2017). What are the best liquidity proxies for global research? Review of Finance, 21(4), 1355–1401. https://doi.org/10.1093/rof/rfx003

Gharib, C., Mefteh-Wali, S., & Jabeur, S. B. (2021). The bubble contagion effect of COVID-19 outbreak: Evidence from crude oil and gold markets. Finance research letters, 38, 101703. https://doi.org/10.1016/j.frl.2020.101703

Glosten, L. R., & Milgrom, P. R. (1985). Bid, ask and transaction prices in a specialist market with heterogeneously informed traders. Journal of Financial Economics, 14, 71–100. https://doi.org/10.1016/0304-405X(85)90044-3

Goodell, J. (2020). COVID-19 and finance: Agendas for future research. Finance Research Letters, 35, 101512. https://doi.org/10.1016/j.frl.2020.101512

Gorton, G., & Metrick, A. (2010). Haircuts. Federal Reserve Bank St Louis Review, 92(6), 507–520. https://doi.org/10.20955/r.92.507-20

Guijarro, F., Moya-Clemente, I., & Saleemi, J. (2019). Liquidity Risk and Investors’ Mood: Linking the Financial Market Liquidity to Sentiment Analysis through Twitter in the S&P500 Index. Sustainability, 11, 7048. https://doi.org/10.3390/su11247048

Guijarro, F., Moya-Clemente, I., & Saleemi, J. (2021). Market Liquidity and Its Dimensions: Linking the Liquidity Dimensions to Sentiment Analysis through Microblogging Data. Journal of Risk and Financial Management, 14(9), 394. https://doi.org/10.3390/jrfm14090394

Huang, R. D., & Stoll, H. R. (1997). The Components of the Bid-Ask Spread: A General Approach. The Review of Financial Studies, 10(4), 995–1034. https://doi.org/10.1093/rfs/10.4.995

Oliveira, N., Cortez, P., & Areal, N. (2017). The impact of microblogging data for stock market prediction: using twitter to predict returns, volatility, trading volume and survey sentiment indices. Expert Systems with Applications, 73, 125-144. https://doi.org/10.1016/j.eswa.2016.12.036

Prokofieva, M. (2015). Twitter-based dissemination of corporate disclosure and the intervening effects of firms’ visibility: Evidence from Australian-listed companies. Journal of Information Systems, 29(2), 107-136. https://doi.org/10.2308/isys-50994

Roll, R. (1984). A Simple Implicit Measure of the Effective Bid‐Ask Spread in an Efficient Market. The Journal of Finance, 39(4), 1127-1139. https://doi.org/10.1111/j.1540-6261.1984.tb03897.x

Saleemi, J. (2020). An estimation of cost-based market liquidity from daily high, low and close prices. Finance, Markets and Valuation, 6(2), 1-11. https://doi.org/10.46503/VUTL1758

Saleemi, J. (2021). COVID-19 and liquidity risk, exploring the relationship dynamics between liquidity cost and stock market returns. National Accounting Review, 3(2), 218-236. https://doi.org/10.3934/NAR.2021011

Saleemi, J. (2022). Asymmetric information modelling in the realized spread: A new simple estimation of the informed realized spread. Finance, Markets and Valuation, 8(1), 1–12. https://doi.org/10.46503/JQYH3943

Sarr, A., & Lybek, T. (2002). Measuring liquidity in financial markets. International Monetary Fund, 2, 1–64. https://doi.org/10.5089/9781451875577.001

Sprenger, T. O., Tumasjan, A., Sandner, P. G., & Welpe, I. M. (2014). Tweets and trades: the information content of stock microblogs. European Financial Management, 20(5), 926-957. https://doi.org/10.1111/j.1468-036X.2013.12007.x

Vidya, C. T., & Prabheesh, K. P. (2020). Implications of COVID-19 pandemic on the global trade networks. Emerging Markets Finance and Trade, 56(10), 2408-2421. https://doi.org/10.1080/1540496X.2020.1785426

Yu, Y., Duan, W., & Cao, Q. (2013). The impact of social and conventional media on firm equity value: A sentiment analysis approach. Decision Support Systems, 55(4), 919-926. https://doi.org/10.1016/j.dss.2012.12.028

Zhang, X., Fuehres, H., & Gloor, P. A. (2011). Predicting stock market indicators through Twitter ‘’i hope it is not as bad as I fear’’. Procedia-Social and Behavioral Sciences, 26, 55-62. https://doi.org/10.1016/j.sbspro.2011.10.562