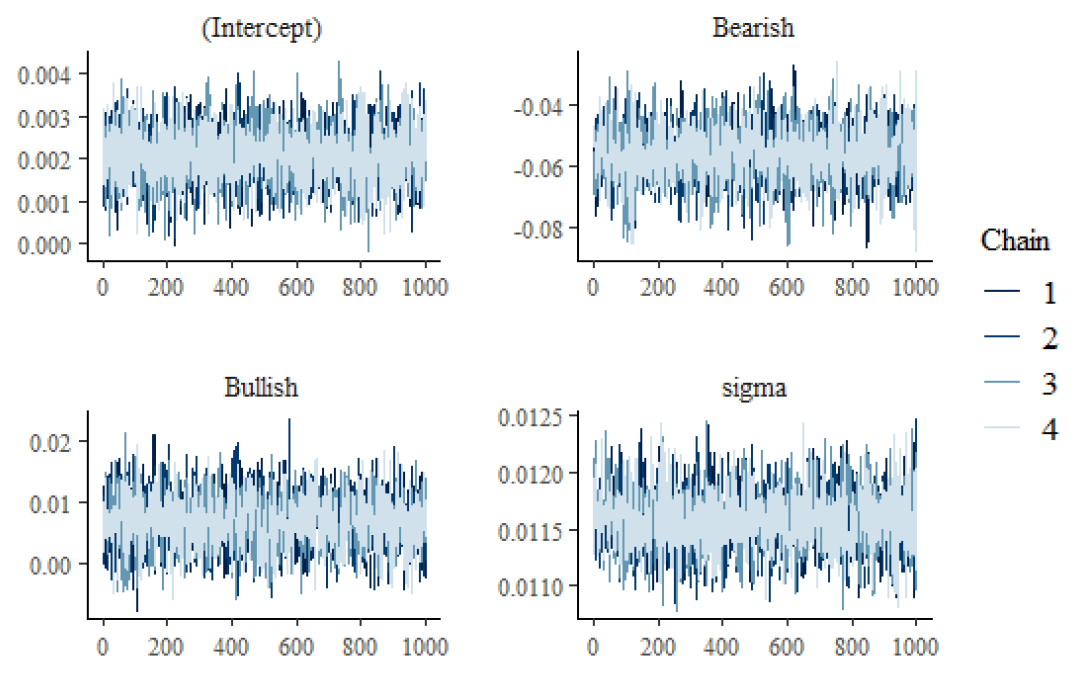

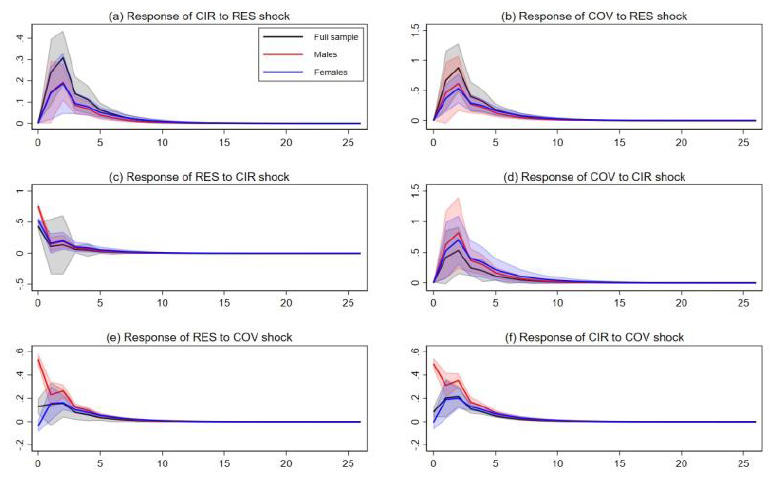

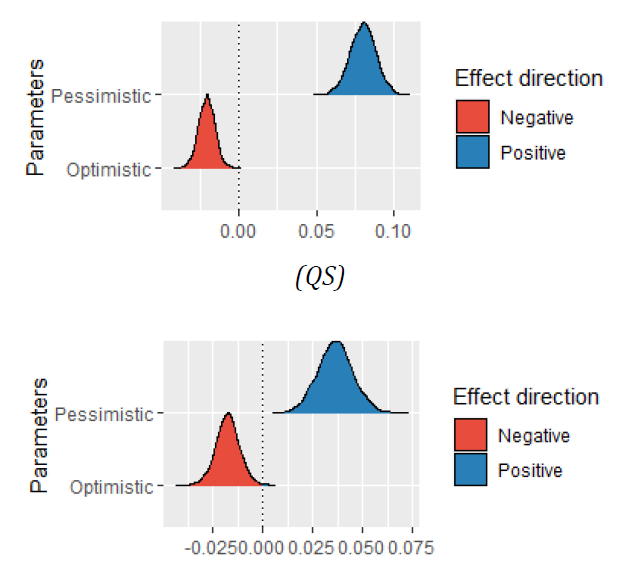

In the behavioral domain, this study discloses the pattern between microblogging-opinionated information and yields on the investment. This phenomenon is particularly related to the political instability in the Pakistan’s economy through the multivariate techniques. Pre-political crisis, the pessimistic sentiments were priced in yields on the investment. In environments of political instability, the intensity of decline in yields was more responsive against an incline in the negative opinions. Meanwhile, the intensity of increase in returns was less responsive against an incline in the positive opinions. The findings were further supported by the Bayesian approach. Before the political instability takes place in the Pakistan’s economy, the occurrence of yields was noted in response to the bearish market period. Post-political instability, there was a higher posterior probability for occurrence of returns against the bearish market period. Conversely, a higher posterior likelihood was noted for occurrence of investment’s yields in response to the bullish market period, but this relevance was not completely probable. From the impulse response analysis, the response of returns was reported against the standard deviation shocks in the microblogging sentiment indicators. The analysis may have potential implications in terms of disclosing the investors’ behavior from a political perspective.

Saleemi, J. (2023). Regime Change Operation in Pakistan: Examining Yield as a Behavioral Pattern of Microblogging rumors during the Political-Obsessed Period. Economic Analysis Letters, 2(2), 20. doi:10.58567/eal02020002

ACS Style

Saleemi, J. Regime Change Operation in Pakistan: Examining Yield as a Behavioral Pattern of Microblogging rumors during the Political-Obsessed Period. Economic Analysis Letters, 2023, 2, 20. doi:10.58567/eal02020002

AMA Style

Saleemi J. Regime Change Operation in Pakistan: Examining Yield as a Behavioral Pattern of Microblogging rumors during the Political-Obsessed Period. Economic Analysis Letters; 2023, 2(2):20. doi:10.58567/eal02020002

Chicago/Turabian Style

Saleemi, Jawad 2023. "Regime Change Operation in Pakistan: Examining Yield as a Behavioral Pattern of Microblogging rumors during the Political-Obsessed Period" Economic Analysis Letters 2, no.2:20. doi:10.58567/eal02020002

Saleemi, J. Regime Change Operation in Pakistan: Examining Yield as a Behavioral Pattern of Microblogging rumors during the Political-Obsessed Period. Economic Analysis Letters, 2023, 2, 20. doi:10.58567/eal02020002

AMA Style

Saleemi J. Regime Change Operation in Pakistan: Examining Yield as a Behavioral Pattern of Microblogging rumors during the Political-Obsessed Period. Economic Analysis Letters; 2023, 2(2):20. doi:10.58567/eal02020002

Chicago/Turabian Style

Saleemi, Jawad 2023. "Regime Change Operation in Pakistan: Examining Yield as a Behavioral Pattern of Microblogging rumors during the Political-Obsessed Period" Economic Analysis Letters 2, no.2:20. doi:10.58567/eal02020002

APA style

Saleemi, J. (2023). Regime Change Operation in Pakistan: Examining Yield as a Behavioral Pattern of Microblogging rumors during the Political-Obsessed Period. Economic Analysis Letters, 2(2), 20. doi:10.58567/eal02020002

Article Metrics

Article Access Statistics

References

Bank, S., Yazar, E. E., & Sivri, U. (2019). Can social media marketing lead to abnormal portfolio returns? European Research on Management and Business Economics, 25, 54-62. doi:10.1016/j.iedeen.2019.04.006

Bartov, E., Faurel, L., & Mohanram, P. (2018). Can Twitter help predict firm-level earnings and stock returns? The Accounting Review, 93(3), 25-27. doi:10.2308/accr-51865

Broadstock, D., & Zhang, D. (2019). Social-media and intraday stock returns: The pricing power of sentiment. Finance Research Letters, 30(C), 116-123. doi:10.1016/j.frl.2019.03.030

Cervelló-Royo, R., & Guijarro, F. (2020). Forecasting stock market trend: a comparison of machine learning algorithms. Finance, Markets and Valuation, 6(1), 37–49. doi:10.46503/NLUF8557

Groß-Klußmann, A., & Hautsch, N. (2011). When machines read the news: Using automated text analytics to quantify high frequency news-implied market reactions. Journal of Empirical Finance, 18(2), 321-340. doi:10.1016/j.jempfin.2010.11.009

Guijarro, F., Moya-Clemente, I., & Saleemi, J. (2019). Liquidity Risk and Investors’ Mood: Linking the Financial Market Liquidity to Sentiment Analysis through Twitter in the S&P500 Index. Sustainability, 11, 7048. doi:10.3390/su11247048

Guijarro, F., Moya-Clemente, I., & Saleemi, J. (2021). Market Liquidity and Its Dimensions: Linking the Liquidity Dimensions to Sentiment Analysis through Microblogging Data. Journal of Risk and Financial Management, 14(9), 394. doi:10.3390/jrfm14090394

Oliveira, N., Cortez, P., & Areal, N. (2013). On the predictability of stock market behavior using stocktwits sentiment and posting volume. In Progress in artificial intelligence. In Lecture notes in computer science, 8154, 355–365. doi:10.1007/978-3-642-40669-0_31

Oliveira, N., Cortez, P., & Areal, N. (2017). The impact of microblogging data for stock market prediction: using twitter to predict returns, volatility, trading volume and survey sentiment indices. Expert Systems with Applications, 73, 125-144. doi:10.1016/j.eswa.2016.12.036

Prokofieva, M. (2015). Twitter-based dissemination of corporate disclosure and the intervening effects of firms’ visibility: Evidence from Australian-listed companies. Journal of Information Systems, 29(2), 107-136. doi:10.2308/isys-50994

Saleemi, J. (2020). In COVID-19 outbreak, correlating the cost-based market liquidity risk to microblogging sentiment indicators. National Accounting Review, 2(3), 249-262. doi:10.3934/NAR.2020014.

Saleemi, J. (2022). Liquidity Pricing Risk and Crude Oil Market: Analyzing the Liquidity as a Priced Factor in Yields during the Pandemic Uncertainty. Journal of Contemporary Research in Business, Economics and Finance, 4(3), 43-55. doi:10.55214/jcrbef.v4i3.183

Smailović, J., Grčar, M., Lavrač, N., & Žnidaršič, M. (2013). Predictive sentiment analysis of Tweets: a stock market application. In Human-Computer Interaction and Knowledge Discovery in Complex, Unstructured, Big Data, 77-88. doi:10.1007/978-3-642-39146-0_8

Sprenger, T. O., Tumasjan, A., Sandner, P. G., & Welpe, I. M. (2014). Tweets and trades: the information content of stock microblogs. European Financial Management, 20(5), 926-957. doi:10.1111/j.1468-036X.2013.12007.x

Wei, C., Shihao, L., & Naqiong, T. (2014). The Influence of Investor Attention on the Stock Return and Risk: An Empirical Study Based on the “Easy Interactive” Platform Data of Shenzhen Stock Exchange. Securities Market Herald, 7, 40-47.