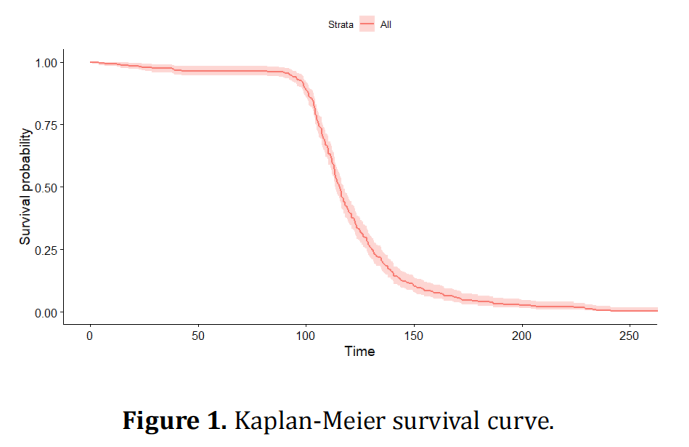

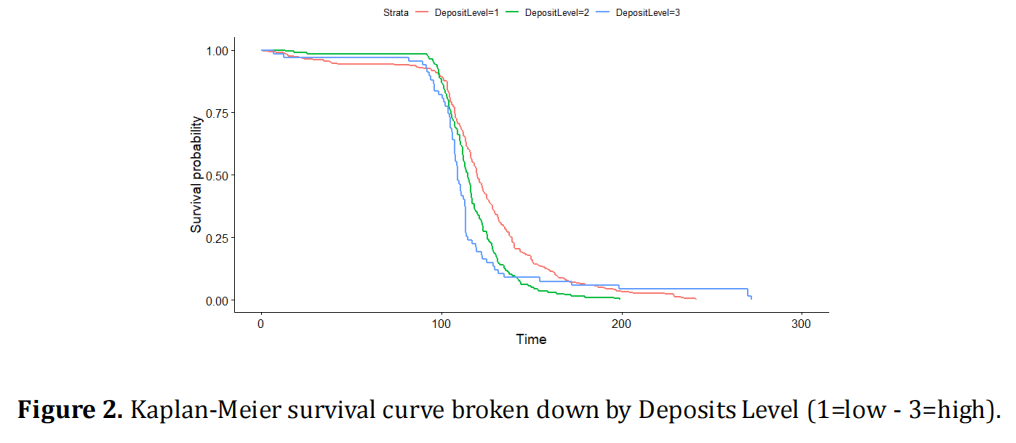

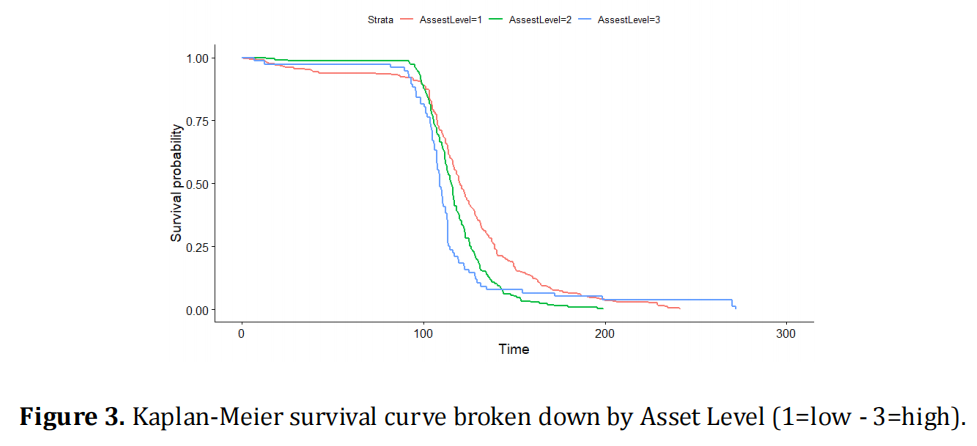

This study investigates the likelihood of time to bank failures in the US between 2001 and April 2023, based on data collected from the Federal Deposit Insurance Corporation's report on "Bank Failures in Brief - Summary 2001 through 2023". The dataset includes 564 instances of bank failures and several variables that may be related to the likelihood of such events, such as asset amount, deposit amount, ADR, deposit level, asset level, inflation rate, short-term interest rates, bank reserves, and GDP growth rate. We explore the efficacy of machine learning survival models in predicting bank failures and compare the performance of different models. Our findings shed light on the factors that may influence the probability of bank failures with a time perspective and provide insights for improving risk management practices in the banking industry.

Vallarino, D. (2024). A Comparative Machine Learning Survival Models Analysis for Predicting Time to Bank Failure in the US (2001-2023). Journal of Economic Analysis, 3(1), 50. doi:10.58567/jea03010007

ACS Style

Vallarino, D. A Comparative Machine Learning Survival Models Analysis for Predicting Time to Bank Failure in the US (2001-2023). Journal of Economic Analysis, 2024, 3, 50. doi:10.58567/jea03010007

AMA Style

Vallarino D. A Comparative Machine Learning Survival Models Analysis for Predicting Time to Bank Failure in the US (2001-2023). Journal of Economic Analysis; 2024, 3(1):50. doi:10.58567/jea03010007

Chicago/Turabian Style

Vallarino, Diego 2024. "A Comparative Machine Learning Survival Models Analysis for Predicting Time to Bank Failure in the US (2001-2023)" Journal of Economic Analysis 3, no.1:50. doi:10.58567/jea03010007

Vallarino, D. A Comparative Machine Learning Survival Models Analysis for Predicting Time to Bank Failure in the US (2001-2023). Journal of Economic Analysis, 2024, 3, 50. doi:10.58567/jea03010007

AMA Style

Vallarino D. A Comparative Machine Learning Survival Models Analysis for Predicting Time to Bank Failure in the US (2001-2023). Journal of Economic Analysis; 2024, 3(1):50. doi:10.58567/jea03010007

Chicago/Turabian Style

Vallarino, Diego 2024. "A Comparative Machine Learning Survival Models Analysis for Predicting Time to Bank Failure in the US (2001-2023)" Journal of Economic Analysis 3, no.1:50. doi:10.58567/jea03010007

APA style

Vallarino, D. (2024). A Comparative Machine Learning Survival Models Analysis for Predicting Time to Bank Failure in the US (2001-2023). Journal of Economic Analysis, 3(1), 50. doi:10.58567/jea03010007

Article Metrics

Article Access Statistics

References

Altman, E. I. (1968). Financial ratios, discriminant analysis and the prediction of corporate bankruptcy. The Journal of Finance, 23(4), 589–609. https://doi.org/10.2307/2978933

Altman, E. I., Marco, G., & Varetto, F. (1994). Corporate distress diag- nosis: comparisons using linear discriminant analysis and neural networks (the Italian experience). Journal of Banking & Finance, 18(3), 505–529. https://doi.org/10.1016/0378-4266(94)90007-8

Andersen, P. K., & Gill, R. D. (1982). Cox’s regression model for counting processes: A large sample study. The Annals of Statistics, 10, 1100–1120.

Ascher, H. (1983). Regression analysis of repairable systems reliability. In Electronic systems effectiveness and life cycle costing (pp. 119–133). Berlin, Heidelberg: Springer. https://doi.org/10.1007/978-3-642-82014-4_8

Back, B., Laitinen, T., & Sere, K. (1996). Neural networks and ge- netic algorithms for bankruptcy predictions. Expert Systems with Applications, 11(4), 407–413. https://doi.org/10.1016/S0957-4174(96)00055-3

Bai, C., Liu, Q., Lu, J., Song, F. M., & Zhang, J. (2004). Corporate governance and market valuation in China. Journal of Comparative Economics, 32(4), 599–616. https://doi.org/10.1016/j.jce.2004.07.00

Balcaen, S., & Ooghe, H. (2006). 35 Years of studies on business failure: an overview of the classical statistical methodologies and their related problems. The British Accounting Review, 38(1), 63–93. https://doi.org/10.1016/j.bar.2005.09.001

Beaver, W. H. (1966). Financial ratios as predictors of failure. Journal of Accounting Research, 4, 71–111. https://doi.org/10.2307/2490171

Bharath, S. T., & Shumway, T. (2008). Forecasting default with the merton distance to default model. Review of Financial Studies, 21(3), 1339–1369. https://doi.org/10.1093/rfs/hhn044

Bijwaard, G. E., Franses, P. H., & Paap, R. (2006). Modeling purchases as repeated events. Journal of Business & Economic Statistics, 24, 487–502. ttps://doi.org/10.1198/073500106000000242

Bonfim, D. (2009). Credit risk drivers: evaluating the contribution of firm level information and of macroeconomic dynamics. Journal of Banking & Finance, 33(2), 281–299. https://doi.org/10.1016/j.jbankfin.2008.08.00

Box-Steffensmeier, J. M., & Boef, S. D. (2006). Repeated events survival models: the conditional frailty model. Statistics in Medicine, 25(20), 3518–3533. https://doi.org/10.1002/sim.2434

Brier, G. W. (1950). Verification of forecasts expressed in terms of probability. Monthly Weather Review, 78(1), 1–3.

Cai, J., & Schaubel, D. E. (2003). Analysis of recurrent event data. Handbook of Statistics, 23, 603–623. https://doi.org/10.1016/S0169-7161(03)23034-0

Carling, T., Pan, D., Ariyan, S., Narayan, D., & Truini, C. (2007). Diagnosis and treatment of interval sentinel lymph nodes in patients with cutaneous melanoma. Plastic and Reconstructive Surgery, 119(3), 907–913.

Chang, S.-H., & Wang, M.-C. (1999). Conditional regression analysis for recurrence time data. Journal of the American Statistical Association, 94(448), 1221–1230. https://doi.org/10.1080/01621459.1999.10473875

Chava, S., & Jarrow, R. A. (2004). Bankruptcy prediction with industry effects. Review of Finance, 8(4), 537–569. https://doi.org/10.1093/rof/8.4.537

Choi, H., Son, H., & Kim, C. (2018). Predicting financial distress of contractors in the construction industry using ensemble learning. Expert Systems with Applications, 110, 1–10. https://doi.org/10.1016/j.eswa.2018.05.026

Choodari-Oskooei, B., Royston, P., & Parmar, M. K. (2012). A simulation study of predictive ability measures in a survival model II: ex- plained randomness and predictive accuracy. Statistics in Medicine, 31(23), 2644–2659. https://doi.org/10.1002/sim.4242

Cielen, A., Peeters, L., & Vanhoof, K. (2004). Bankruptcy prediction using a data envelopment analysis. European Journal of Operational Research, 154(2), 526–532. https://doi.org/10.1016/S0377-2217(03)00186-3

Clayton, D. (1994). Some approaches to the analysis of recurrent event data. Statistical Methods in Medical Research, 3(3), 244–262. https://doi.org/10.1177/096228029400300304

Deakin, E. B. (1972). A discriminant analysis of predictors of business failure. Journal of Accounting Research, 3(3), 167–179. https://doi.org/10.2307/2490225

Dimitras, A. I., Slowinski, R., Susmaga, R., & Zopounidis, C. (1999). Business failure prediction using rough sets. European Journal of Operational Research, 114(2), 263–280. https://doi.org/10.1016/S0377-2217(98)00255-0

du Jardin, P. (2017). Dynamics of firm financial evolution and bankruptcy prediction. Expert Systems with Applications, 75, 25–43. https://doi.org/10.1016/j.eswa.2017.01.016

Duffie, D., Saita, L., & Wang, K. (2007). Multi-period corporate default prediction with stochastic covariates. Journal of Financial Economics, 83(3), 635–665. https://doi.org/10.1016/j.jfineco.2005.10.011

Edmister, R. O. (1972). An empirical test of financial ratio analy- sis for small business failure prediction. Journal of Financial and Quantitative Analysis, 7(2), 1477–1493. doi:10.2307/2329929

Ejoku, J., Odhiambo, C., & Chaba, L. (2020). Analysis of recurrent events with associated informative censoring: Application to HIV data. International Journal of Statistics in Medical Research, 9(21).

Geng, R., Bose, I., & Chen, X. (2015). Prediction of financial distress: an empirical study of listed Chinese companies using data mining. European Journal of Operational Research, 241(1), 236–247. https://doi.org/10.1016/j.ejor.2014.08.016

Gepp, A., & Kumar, K. (2008). The role of survival analysis in financial distress prediction. International Research Journal of Finance and Economics, 16(16), 13–34.

Gilson, S. C. (1989). Management turnover and financial distress. Journal of Financial Economics, 25(2), 241–262. https://doi.org/10.1016/0304-405X(89)90083-4

Godlewski, C. J. (2015). The dynamics of bank debt renegotiation in Europe: A survival analysis approach. Economic Modelling, 49, 19–31. https://doi.org/10.1016/j.econmod.2015.03.017

Gönen, M., & Heller, G. (2005). Concordance probability and discrimi- natory power in proportional hazards regression. Biometrika, 92(4), 965–970. https://doi.org/10.1093/biomet/92.4.965

Graf, E., Schmoor, C., Sauerbrei, W., & Schumacher, M. (1999). As- sessment and comparison of prognostic classification schemes for survival data. Statistics in Medicine, 18(17–18), 2529–2545. https://doi.org/10.1002/(SICI)1097-0258(19990915/30)18:17/18<2529::AID-SIM274>3.0.CO;2-5

Graf, E., & Schumacher, M. (1995). An investigation on measures of explained variation in survival analysis. Journal of the Royal Statistical Society. Series D, 44(4), 497–507. https://doi.org/10.2307/2348898

Harrell Jr, F. E., Lee, K. L., & Mark, D. B. (1996). Multivariable prognostic models: issues in developing models, evaluating assumptions and adequacy, and measuring and reducing errors. Statistics in Medicine, 15(4), 361–387. https://doi.org/10.1002/(SICI)1097-0258(19960229)15:4<361::AID-SIM168>3.0.CO;2-4

Henriques, I. C., Sobreiro, V. A., Kimura, H., & Mariano, E. B. (2020). Two-stage DEA in banks: Terminological controversies and future directions. Expert Systems with Applications, 161, 113632. https://doi.org/10.1016/j.eswa.2020.113632

Hosaka, T. (2019). Bankruptcy prediction using imaged financial ratios and convolutional neural networks. Expert Systems with Applications, 117, 287–299. https://doi.org/10.1016/j.eswa.2018.09.039

Hu, Y. C., & Ansell, J. (2007). Measuring retail company performance using credit scoring techniques. European Journal of Operational Research, 183(3), 1595–1606. https://doi.org/10.1016/j.ejor.2006.09.101

Hu, D., & Zheng, H. (2015). Does ownership structure affect the degree of corporate financial distress in China? Journal of Accounting in Emerging Economies, 5(1), 35–50. https://doi.org/10.1108/JAEE-09-2011-0037

Hua, Z., Wang, Y., Xu, X., Zhang, B., & Liang, L. (2007). Predicting corporate financial distress based on integration of support vector machine and logistic regression. Expert Systems with Applications, 33(2), 434–440. https://doi.org/10.1016/j.eswa.2006.05.006

Jiang, Y., & Jones, S. (2018). Corporate distress prediction in China: a machine learning approach. Account Finance, 58, 1063–1109. https://doi.org/10.1111/acfi.12432

Jiang, S. T., Landers, T. L., & Reed Rhoads, T. (2006). Proportional intensity models robustness with overhaul intervals. Quality and Reliability Engineering International, 22(3), 251–263. https://doi.org/10.1002/qre.713

John, T. A. (1993). Accounting measures of corporate liquidity, leverage, and costs of financial distress. Financial Management, 22(3), 91–100. https://doi.org/10.2307/3665930

Kahl, M. (2002). Economic distress, financial distress, and dynamic liquidation. The Journal of Finance, 57(1), 135–168. https://doi.org/10.1111/1540-6261.00418

Kam, A., Citron, D., & Muradoglu, G. (2010). Financial distress resolution in China – two case studies. Qualitative Research in Financial Markets, 2(2), 46–79. https://doi.org/10.1108/17554171011053667

Kaplan, E. L., & Meier, P. (1958). Nonparametric estimation from in- complete observations. Journal of the American Statistical Association, 53(282), 457–481. https://doi.org/10.1080/01621459.1958.10501452

Kim, M., Ma, S., & Zhou, Y. (2016). Survival prediction of distressed firms: evidence from the Chinese special treatment firms. Journal of the Asia Pacific Economy, 21(3), 418–443. https://doi.org/ 10.1080/13547860.2016.1176645

Kristanti, Farida Titik, & Herwany, Aldrin (2017). Corporate governance, financial ratios, political risk and financial distress: A survival analysis. Accounting and Finance Review, 2(2), 26–34.

Kuhnen, C. M., & Melzer, B. T. (2018). Noncognitive abilities and financial delinquency: the role of self-efficacy in avoiding financial distress. The Journal of Finance, 73(6), 2837–2869. https://doi.org/10.1111/jofi.12724

Kumar, P. R., & Ravi, V. (2007). Bankruptcy prediction in banks and firms via statistical and intelligent techniques – a review. European Journal of Operational Research, 180(1), 1–28. https://doi.org/10.1016/j.ejor.2006.08.043

Lacher, R. C., Coats, P. K., Sharma, S. C., & Fant, L. F. (1995). A neural network for classifying the financial health of a firm. European Journal of Operational Research, 85(1), 53–65. https://doi.org/10.1016/0377-2217(93)E0274-2

Lane, W. R., Looney, S. W., & Wansley, J. W. (1986). An application of the cox proportional hazards model to bank failure. Journal of Banking & Finance, 10(4), 511–531. https://doi.org/10.1016/S0378-4266(86)80003-6

Lee, M. C. (2014). Business bankruptcy prediction based on survival analysis approach. International Journal of Computer Science & Information Technology, 6(2), 103. https://doi.org/10.5121/ijcsit.2014.6207

Leonardis, D. D., & Rocci, R. (2008). Assessing the default risk by means of a discrete – time survival analysis approach. Applied Stochastic Models in Business and Industry, 24(4), 291–306. https://doi.org/10.1002/asmb.705

Leong, R. W., Nguyen, N., Meredith, C. G., et al. (2008). In vivo confocal endomicroscopy in the diagnosis and evaluation of celiac disease. Gastroenterology, 135(6), 1870–1876. https://doi.org/10.1053/j.gastro.2008.08.054

Li, Z., Crook, J., & Andreeva, G. (2014). Chinese companies distress prediction: an application of data envelopment analysis. Journal of the Operational Research Society, 65(3), 466–479. https://doi.org/10.1057/jors.2013.67

Li, Z., Crook, J., & Andreeva, G. (2017). Dynamic prediction of financial distress using Malmquist DEA. Expert Systems with Applications, 80, 94–106. https://doi.org/10.1016/j.eswa.2017.03.017

Li, Z., Crook, J., Andreeva, G., & Tang, Y. (2021). Predicting the risk of fi- nancial distress using corporate governance measures. Pacific-Basin Finance Journal, 68, Article 101334. https://doi.org/10.1016/j.pacfin.2020.101334

Li, H., Wang, Z., & Deng, X. (2008). Ownership, independent direc- tors, agency costs and financial distress: evidence from Chinese listed companies. Corporate Governance: The International Journal of Business in Society, 8(5), 622–636. https://doi.org/10.1108/14720700810913287

Luoma, M., & Laitinen, E. K. (1991). Survival analysis as a tool for company failure prediction. Omega, 19(6), 673–678. https://doi.org/10.1016/0305-0483(91)90015-L

Mai, F., Tian, S., Lee, C., & Ma, L. (2019). Deep learning models for bankruptcy prediction using textual disclosures. European Journal of Operational Research, 274(2), 743–758. https://doi.org/10.1016/j.ejor.2018.10.024

Mantel, N. (1966). Evaluation of survival data and two new rank order statistics arising in its consideration. Cancer Chemother Rep, 50(3), 163–170.

Martin, D. (1977). Early warning of bank failure: a logit regression approach. Journal of Banking & Finance, 1(3), 249–276. https://doi.org/10.1016/0378-4266(77)90022-X

Merton, R. C. (1974). On the pricing of corporate debt: the risk structure of interest rates. The Journal of Finance, 29(2), 449–470. https://doi.org/10.2307/2978814

Min, J. H., & Lee, Y. C. (2005). Bankruptcy prediction using support vector machine with optimal choice of kernel function parameters. Expert Systems with Applications, 28(4), 603–614. https://doi.org/10.1016/j.eswa.2004.12.008

Moulton, L. H., & Dibley, M. J. (1997). Multivariate time-to-event models for studies of recurrent childhood diseases. International Journal of Epidemiology, 26(6), 1334–1339. https://doi.org/10.1093/ije/26.6.1334

Ohlson, J. A. (1980). Financial ratios and the probabilistic prediction of bankruptcy. Journal of Accounting Research, 18(1), 109–131. https://doi.org/10.2307/2490395

O’Neill, H. M. (1986). Turnaround and recovery: What strategy do you need? Long Range Planning, 19(1), 80–88. https://doi.org/10.1016/0024-6301(86)90131-7

Paradi, J. C., Asmild, M., & Simak, P. C. (2004). Using DEA and worst practice DEA in credit risk evaluation. Journal of Productivity Analysis, 21(2), 153–165. https://doi.org/10.1023/B:PROD.0000016870.47060.0b

Parker, S., Peters, G. F., & Turetsky, H. F. (2005). Corporate governance factors and auditor going concern assessments. Review of Accounting and Finance, 4(3), 5–29. https://doi.org/10.1108/eb043428

Peña, E. A., Slate, E. H., & González, J. R. (2007). Semiparametric inference for a general class of models for recurrent events. Journal of Statistical Planning and Inference, 137(6), 1727–1747. https://doi.org/10.1016/j.jspi.2006.05.004

Pfennig, A., Schlattmann, P., Alda, M., Grof, P., Glenn, T., Müller- Oerlinghausen, B., et al. (2010). Influence of atypical features on the quality of prophylactic effectiveness of long-term lithium treatment in bipolar disorders. Bipolar Disorders, 12(4), 390–396. https://doi.org/10.1111/j.1399-5618.2010.00826.x

Platt, H. D., & Platt, M. B. (2002). Predicting corporate financial distress: Reflections on choice-based sample bias. Journal of Economics and Finance, 26(2), 184–199. https://doi.org/10.1007/BF02755985

Prentice, R. L., Williams, B. J., & Peterson, A. V. (1981). On the regression analysis of multivariate failure time data. Biometrika, 68, 373–389. https://doi.org/10.1093/biomet/68.2.373

Rahman, M. S., Ambler, G., Choodari-Oskooei, B., & Omar, R. Z. (2017). Review and evaluation of performance measures for survival pre- diction models in external validation settings. BMC Medical Research Methodology, 17(1), 60. https://doi.org/10.1186/s12874-017-0336-2

Schemper, M., & Stare, J. (1996). Explained variation in survival analysis. Statistics in Medicine, 15(19), 1999–2012. https://doi.org/10.1002/(SICI)1097-0258(19961015)15:19<1999::AID-SIM353>3.0.CO;2-D

Shumway, T. (2001). Forecasting bankruptcy more accurately: a simple hazard model. Journal of Business, 74(1), 101–124. https://www.jstor.org/stable/10.1086/209665

Sun, J., Jia, M. Y., & Li, H. (2011). Adaboost ensemble for finan- cial distress prediction: an empirical comparison with data from Chinese listed companies. Expert Systems with Applications, 38(8), 9305–9312. https://doi.org/10.1016/j.eswa.2011.01.042

Tam, K. Y., & Kiang, M. Y. (1992). Managerial applications of neural networks: the case of bank failure predictions. Management Science, 38(7), 926–947. https://doi.org/10.1287/mnsc.38.7.926

Tinoco, M. H., & Wilson, N. (2013). Financial distress and bankruptcy prediction among listed companies using accounting, market and macroeconomic variables. International Review of Financial Analysis, 30, 394–419. https://doi.org/10.1016/j.irfa.2013.02.013

Twisk, J., Smidt, N., & de Vente, W. (2005). Applied analysis of recurrent events: a practical overview. Journal of Epidemiology and Community Health, 59, 706–710. http://dx.doi.org/10.1136/jech.2004.030759

Uno, H., Cai, T., Pencina, M. J., D’Agostino, R. B., & Wei, L. J. (2011). On the C-statistics for evaluating overall adequacy of risk predic- tion procedures with censored survival data. Statistics in Medicine, 30(10), 1105–1117. https://doi.org/10.1002/sim.4154

Verikas, A., Kalsyte, Z., Bacauskiene, M., & Gelzinis, A. (2010). Hybrid and ensemble-based soft computing techniques in bankruptcy prediction: a survey. Soft Computing, 14(9), 995–1010. https://doi.org/10.1007/s00500-009-0490-5

Wang, Y. L., & Carson, J. (2010). Macroeconomic factors and insurer rating transitions. Forensic Economics EJournal. Wang, Yuling and Carson, James M., Macroeconomic Factors and Insurer Rating Transitions (February 14, 2010). http://dx.doi.org/10.2139/ssrn.1558456

Wang, Z., & Deng, X. (2006). Corporate governance and financial distress. The Chinese Economy, 39(5), 5–27. https://doi.org/10.2753/CES1097-1475390501

Wang, Z., & Li, H. (2007). Financial distress prediction of Chinese listed companies: a rough set methodology. Chinese Management Studies, 1(2), 93–110. https://doi.org/10.1108/17506140710758008

Wei, L. J., Lin, D. Y., & Weissfeld, L. (1989). Regression analysis of multivariate incomplete failure time data by modelling marginal distributions. Journal of the American Statistical Association, 84(408), 1065–1073. https://doi.org/10.1080/01621459.1989.10478873

Wruck, K. H. (1990). Financial distress, reorganization, and or- ganizational efficiency. Journal of Financial Economics, 27(2), 419–444. https://doi.org/10.1016/0304-405X(90)90063-6

Wu, D., Liang, L., & Yang, Z. (2008). Analysing the financial distress of Chinese public companies using probabilistic neural networks and multivariate discriminate analysis. Socio-Economic Planning Sciences, 42(3), 206–220. https://doi.org/10.1016/j.seps.2006.11.002

Yang, Z., You, W., & Ji, G. (2011). Using partial least squares and support vector machines for bankruptcy prediction. Expert Systems with Applications, 38(7), 8336–8342. https://doi.org/10.1016/j.eswa.2011.01.021

Zhou, F., Fu, L., Li, Z., & Xu, J. (2022). The recurrence of financial distress: A survival analysis. International Journal of Forecasting, 38(3), 1100-1115. https://doi.org/10.1016/j.ijforecast.2021.12.005