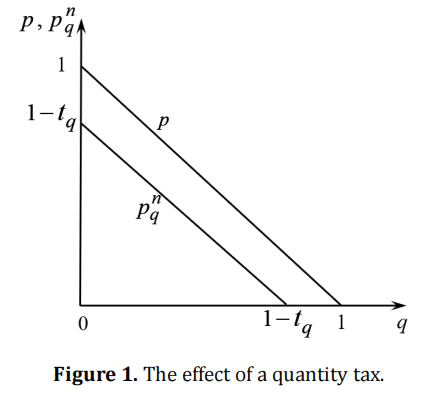

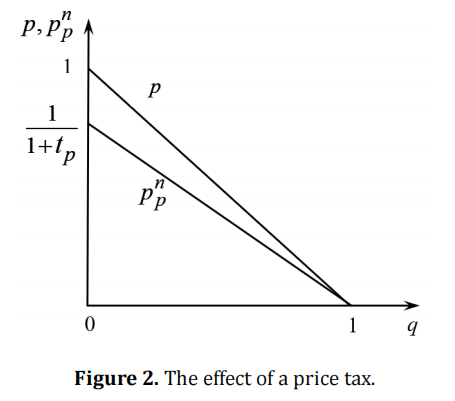

In reality firms most often face negatively sloped demand curves. Then, for a given level of consumers’ surplus, levies on prices yield higher fiscal revenues than specific duties. Therefore, according to the prevailing view, the switch from unit to ad valorem taxation is supposed to generate more welfare; some even speak of an associated Pareto-improvement. However, this is not true because taxing prices merely transfers profits to the Treasury, while total rent remains unaffected. Since excise duties diminish the welfare gain in comparison with untaxed trade, an appropriately designed income tax allows all parties to benefit. Sales should be taxed only exceptionally.

Helmedag, F. Welfare Effects of Commodity Taxation. Journal of Economic Analysis, 2023, 2, 22. doi:10.58567/jea02020001

AMA Style

Helmedag F. Welfare Effects of Commodity Taxation. Journal of Economic Analysis; 2023, 2(2):22. doi:10.58567/jea02020001

Chicago/Turabian Style

Helmedag, Fritz 2023. "Welfare Effects of Commodity Taxation" Journal of Economic Analysis 2, no.2:22. doi:10.58567/jea02020001

APA style

Helmedag, F. (2023). Welfare Effects of Commodity Taxation. Journal of Economic Analysis, 2(2), 22. doi:10.58567/jea02020001

Article Metrics

Article Access Statistics

References

Anderson, S. P., A. de Palma and B. Kreider (2001), The efficiency of indirect taxes under imperfect competition, Journal of Public Economics 81, 231-251. https://doi.org/10.1016/S0047-2727(00)00085-2

Atkinson, A. and J. Stiglitz (1976), The Design of Tax Structure: Direct Versus Indirect Taxation, Journal of Public Economics 6, 55-75. https://doi.org/10.1016/0047-2727(76)90041-4

Bundesfinanzhof (2015). Urteil vom 7.7.2015, VII R 65/13. https://openjur.de/u/2246340.html.

Bundesministerium der Finanzen (2021). Steuereinnahmen nach Steuergruppen 2019-2020. https://www. bundesfinanzministerium.de/Content/DE/Standardartikel/Themen/Steuern/Steuerschaetzungen_und_Steuereinnahmen/2021-09-22-steuereinnahmen-nach-steuergruppen-2019-2020.pdf?__blob=publicationFile&v=2.

Engel, E. (1857), Die vorherrschenden Gewerbszweige in den Gerichtsämtern mit Beziehung auf die Productions- und Consumtionsverhältnisse des Königreichs Sachsen, Zeitschrift des Statistischen Bureaus des Königlich Sächsischen Ministeriums des Innern 3, Nr. 8/9, 153-184. https://www.econstor.eu/handle/10419/233572

Helmedag, F. (1982), Zur Diskussion und Konstruktion von Gutenbergs doppelt geknickter Preis-Absatzfunktion, Jahrbücher für Nationalökonomie und Statistik 197, 545-564. https://doi.org/10.1515/jbnst-1982-0606

Helmedag, F. (2012), Individuelle und kollektive Gewinnmaximierung auf homogenen Märkten, in Oberender, P. (ed.), Private und öffentliche Kartellrechtsdurchsetzung (S. 9-38). Berlin Duncker & Humblot. https://www.tu-chemnitz.de/wirtschaft/vwl2/downloads/wettbew/HomogeneMaerkte10.pdf

Helmedag, F. (2018), Warenproduktion mittels Waren, Zur Rehabilitation des Wertgesetzes, 3rd ed., Marburg Metropolis.

Helmedag, F. (2019), Marx and Keynes: from exploitation to employment, European Journal of Economics and Economic Policies: Intervention 16, 260-271. https://doi.org/10.4337/ejeep.2019.0048

Hoffmann, M. and M. Runkel (2016), A welfare comparison of ad valorem and unit tax regimes, International Tax & Public Finance 23, 140-157. https://doi.org/10.1007/s10797-015-9355-2

Kiser, E. and S. M. Karceski (2017), Political Economy of Taxation, Annual Review of Political Science 20, 75-92. https://doi.org/10.1146/annurev-polisci-052615-025442

Li, H. and X. Liu (2021), Ad valorem versus per unit taxation: a perspective from price signaling, Journal of Economics 134, 27-47. https://doi.org/10.1007/s00712-021-00736-w

Saez, E. (2002), The desirability of commodity taxation under non-linear income taxation and heterogeneous tastes, Journal of Public Economics 83, 217-230. https://doi.org/10.1016/S0047-2727(00)00159-6

Schwabe, H. (1879), Das Verhältniß von Miethe und Einkommen in Berlin, Beiträge zu einer Consumtionsstatistik, in Statistisches Bureau der Stadt Berlin (ed.), Gemeinde-Kalender und städtisches Jahrbuch für 1868 2, 264 -267.

Skeath, S. and G. Trandel (1994), A Pareto comparison of ad valorem and unit taxes in noncompetitive environments, Journal of Public Economics 53, 53-71. https://doi.org/10.1016/0047-2727(94)90013-2

Stewart, M. (2022), Tax and Government in the Twenty-First Century, Cambridge University Press.

Stiglitz, J. (2000). Economics of the Public Sector. 3rd ed., New York / London W. Norton & Company.

Suits, D. and R. Musgrave (1953), Ad Valorem and Unit Taxes Compared, Quarterly Journal of Economics 67, 598-604. https://doi.org/10.2307/1883604

Wicksell, K. (1896), Finanztheoretische Untersuchungen nebst Darstellung und Kritik des Steuerwesens Schwedens, Jena Gustav Fischer.