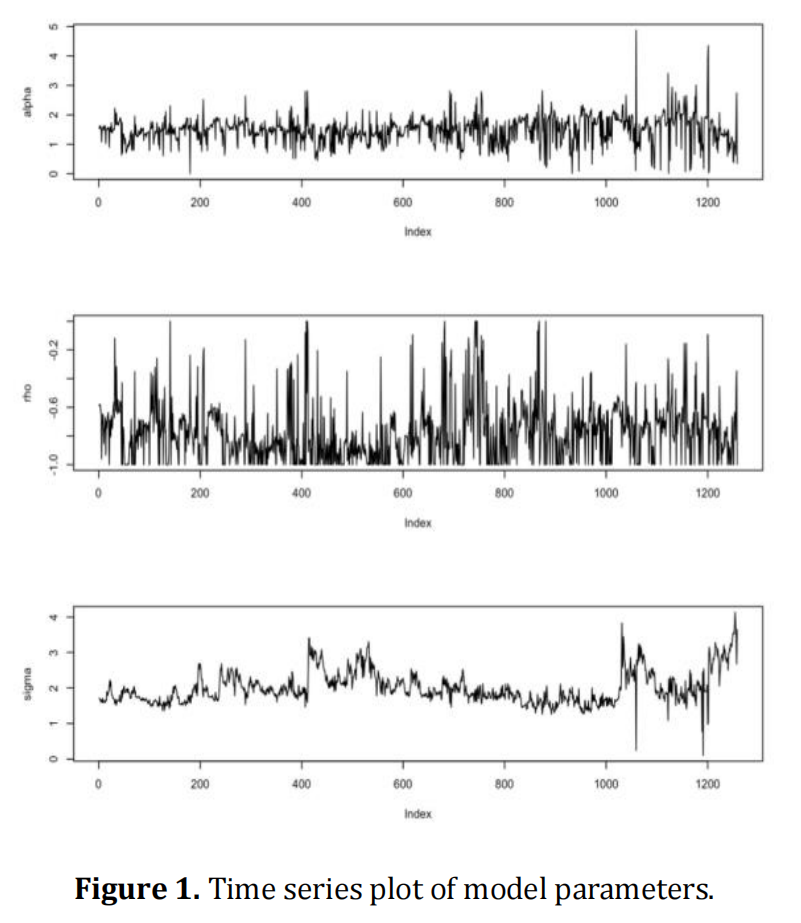

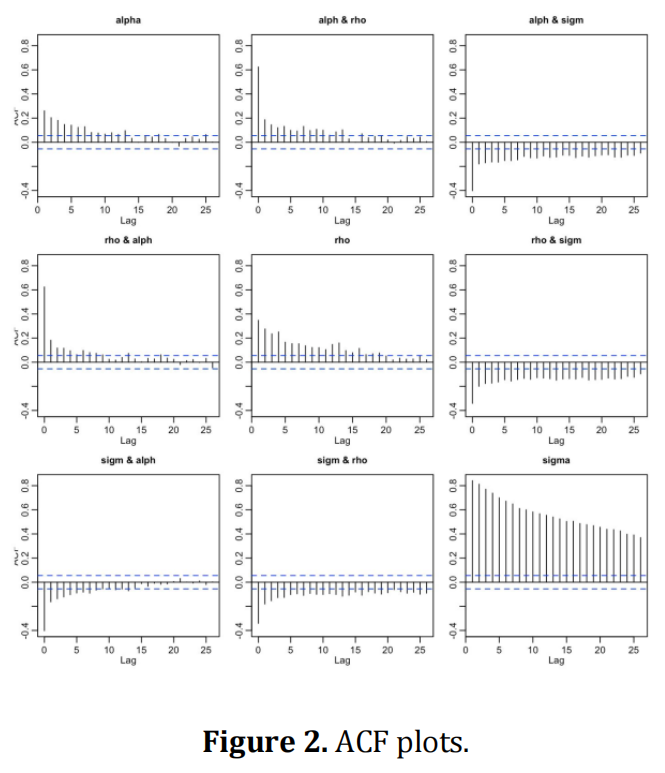

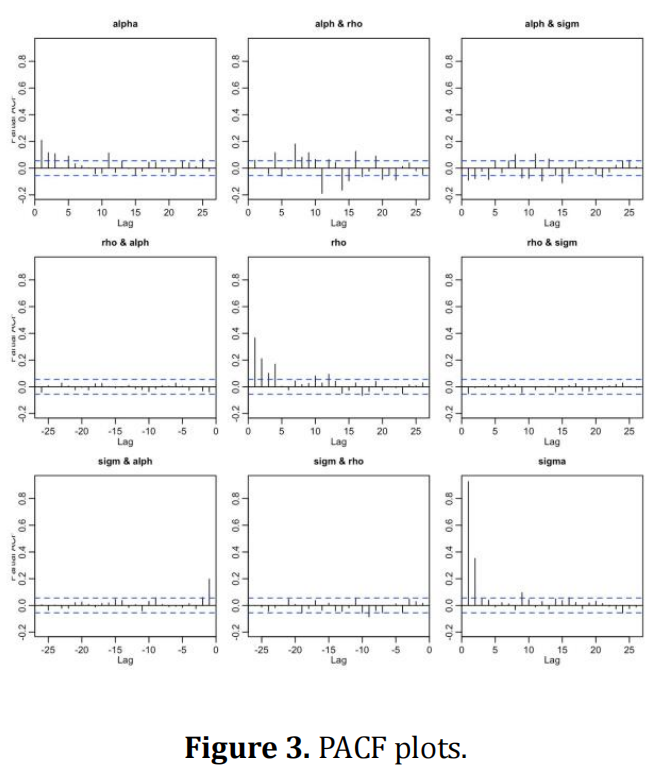

We present two approaches to forecasting parameters in the SABR model. The first approach is the vector autoregressive moving-average model (VARMA) for the time series of the in-sample calibrated parameters, and the second is based on machine learning techniques called epsilon-support vector regression (ε-SVR). Using daily data of S&P 500 ETF option prices from January 1, 2014, to December 31, 2018, we first calibrate the daily values of the model parameters from the training sample, then conduct out-of-sample forecasting of parameters and pricing of options. Both approaches produce good fits between the forecasted and calibrated parameters for out-of-sample dates. A comparison study shows that using forecasted parameters as inputs, the SABR model generates better pricing results than assuming constant parameters or using lag parameters. We also discuss the market conditions under which one approach outperforms the other.

Chen, L.; Zhu, J.; Yang, C. Forecasting Parameters in the SABR Model. Journal of Economic Analysis, 2022, 1, 6. doi:10.58567/jea01010005

AMA Style

Chen L, Zhu J, Yang C. Forecasting Parameters in the SABR Model. Journal of Economic Analysis; 2022, 1(1):6. doi:10.58567/jea01010005

Chicago/Turabian Style

Chen, Li; Zhu, Jianing; Yang, Cunyi 2022. "Forecasting Parameters in the SABR Model" Journal of Economic Analysis 1, no.1:6. doi:10.58567/jea01010005

APA style

Chen, L., Zhu, J., & Yang, C. (2022). Forecasting Parameters in the SABR Model. Journal of Economic Analysis, 1(1), 6. doi:10.58567/jea01010005

Article Metrics

Article Access Statistics

References

Bin, C. (2007). Calibration of the Heston model with application in derivative pricing and hedging. Master's thesis, Department of Mathematics, Technical University of Delft, Delft, The Netherlands. http://ta.twi.tudelft.nl/mf/users/oosterle/oosterlee/chen.pdf

Chen, N., and Yang, N. (2019). The principle of not feeling the boundary for the SABR model. Quantitative Finance 19, 427-436. https://doi.org/10.1080/14697688.2018.1486037

Choi, J., and Wu, L. (2021). The equivalent constant-elasticity-of-variance (CEV) volatility of the stochastic-alpha-beta-rho (SABR) model. Journal of Economic Dynamics & Control 128. https://doi.org/10.1016/j.jedc.2021.104143

Cui, Y., Del Bano Rollin, S., and Germano, G. (2017). Full and fast calibration of the Heston stochastic volatility model. European Journal of Operational Research 263, 625-638. https://doi.org/10.1016/j.ejor.2017.05.018

Gulisashvili, A., Horvath, B., and Jacquier, A. (2018). Mass at zero in the uncorrelated SABR model and implied volatility asymptotics. Quantitative Finance 18, 1753-1765. https://doi.org/10.1080/14697688.2018.1432883

Hagan, P.S., Kumar, D., Lesniewski, A., and Woodward, D. (2014). Arbitrage‐free SABR. Wilmott 2014, 60-75. https://doi.org/10.1002/wilm.10290

Horvath, B., and Reichmann, O. (2018). Dirichlet Forms and Finite Element Methods for the SABR Model. Siam Journal on Financial Mathematics 9, 716-754. https://doi.org/10.1137/16M1066117

Leitao, A., Grzelak, L.A., and Oosterlee, C.W. (2017). On a one time-step Monte Carlo simulation approach of the SABR model: Application to European options. Applied Mathematics and Computation 293, 461-479. https://doi.org/10.1016/j.amc.2016.08.030

Panigrahi, S.S., Mantri, J.K., and Ieee (2015). Epsilon-SVR and Decision Tree for Stock Market Forecasting. International Conference on Green Computing and Internet of Things (ICGCIoT), 761-766. https://ieeexplore.ieee.org/abstract/document/7380565/

Thakoor, N., Tangman, D.Y., and Bhuruth, M. (2019). A Spectral Approach to Pricing of Arbitrage-Free SABR Discrete Barrier Options. Computational Economics 54, 1085-1111. https://doi.org/10.1007/s10614-018-9868-8

Yang, N., and Wan, X. (2018). The survival probability of the SABR model: asymptotics and application. Quantitative Finance 18, 1767-1779. https://doi.org/10.1080/14697688.2017.1422083

Yang, N., Chen, N., Liu, Y., and Wan, X. (2017). Approximate arbitrage-free option pricing under the SABR model. Journal of Economic Dynamics & Control 83, 198-214. https://doi.org/10.1016/j.jedc.2017.08.004

Zhang, M., and Fabozzi, F.J. (2016). On the Estimation of the SABR Model's Beta Parameter: The Role of Hedging in Determining the Beta Parameter. Journal of Derivatives, 24, 48-57. https://doi.org/10.3905/jod.2016.24.1.048

Zhang, N. (2011). Properties of the SABR model. Working Paper. https://www.diva-portal.org/smash/get/diva2:430537/FULLTEXT01.pdf