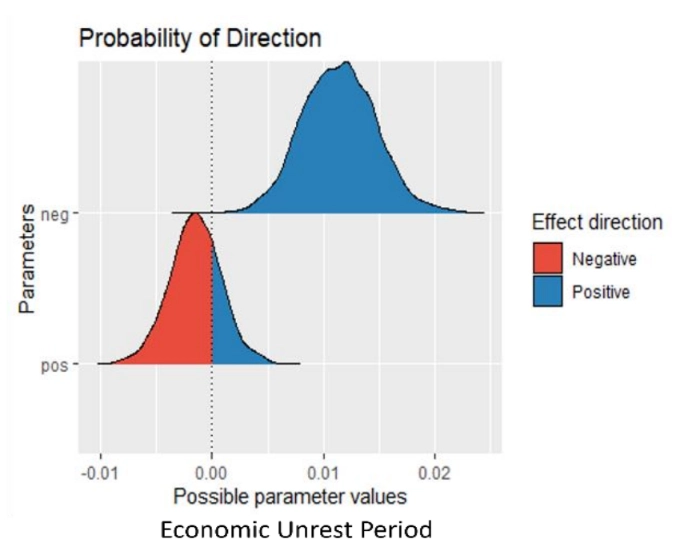

Excessive volatility in financial markets can disrupt economic activity, affect investor and consumer confidence, and potentially lead to financial crises in an economy. Due to this backdrop, this study examined the link between asset class volatility and the output gap in Nigeria. The asset classes were categorized into stock, crude, gold, and bitcoin. The study adopted the GARCH and Bayesian VAR approach and found that all share index has an initial negative impulse with output gap while other asset classes have a positive impulse on output gap. The outcome of this study revealed to both policymakers and economists the potential risks and vulnerabilities of asset class volatility in the economy. Based on this result, recommendations are made amongst which is the strengthening of the Nigerian stock market to help with the inflationary pressures this is because the Nigerian stock market hurt the output gap also, the government should prioritize investing in crude, gold, and bitcoin to push the actual output to full capacity, which brings about employment.

umeokwobi, r., Awujola, A., Nkoro, E., & Aigbedion, M. (2024). Nexus Between Asset Class Volatility and the Output Gap in Nigeria: A Bayesian Var Approach. Financial Economics Letters, 3(1), 25. doi:10.58567/fel03010004

ACS Style

umeokwobi, r.; Awujola, A.; Nkoro, E.; Aigbedion, M. Nexus Between Asset Class Volatility and the Output Gap in Nigeria: A Bayesian Var Approach. Financial Economics Letters, 2024, 3, 25. doi:10.58567/fel03010004

AMA Style

umeokwobi r, Awujola A, Nkoro E et al.. Nexus Between Asset Class Volatility and the Output Gap in Nigeria: A Bayesian Var Approach. Financial Economics Letters; 2024, 3(1):25. doi:10.58567/fel03010004

Chicago/Turabian Style

umeokwobi, richard; Awujola, Abayomi; Nkoro, Emeka; Aigbedion, Marvelous 2024. "Nexus Between Asset Class Volatility and the Output Gap in Nigeria: A Bayesian Var Approach" Financial Economics Letters 3, no.1:25. doi:10.58567/fel03010004

Share and Cite

ACS Style

umeokwobi, r.; Awujola, A.; Nkoro, E.; Aigbedion, M. Nexus Between Asset Class Volatility and the Output Gap in Nigeria: A Bayesian Var Approach. Financial Economics Letters, 2024, 3, 25. doi:10.58567/fel03010004

AMA Style

umeokwobi r, Awujola A, Nkoro E et al.. Nexus Between Asset Class Volatility and the Output Gap in Nigeria: A Bayesian Var Approach. Financial Economics Letters; 2024, 3(1):25. doi:10.58567/fel03010004

Chicago/Turabian Style

umeokwobi, richard; Awujola, Abayomi; Nkoro, Emeka; Aigbedion, Marvelous 2024. "Nexus Between Asset Class Volatility and the Output Gap in Nigeria: A Bayesian Var Approach" Financial Economics Letters 3, no.1:25. doi:10.58567/fel03010004

APA style

umeokwobi, r., Awujola, A., Nkoro, E., & Aigbedion, M. (2024). Nexus Between Asset Class Volatility and the Output Gap in Nigeria: A Bayesian Var Approach. Financial Economics Letters, 3(1), 25. doi:10.58567/fel03010004

Article Metrics

Article Access Statistics

References

Adigun, A. O., & Okhankhuele, O. T. (2021). Stock market, money supply and industrial output in Nigeria. Fuoye Journal of Finance and Contemporary Issue, 1(1), 103-110. https://fjfci.fuoye.edu.ng/index.php/fjfci/article/view/13.

Aharon, D., & Demir, E. (2022). NFTs and asset class spill overs: lessons from the period around the covid-19 pandemic. Finance Research Letters. (47). https://doi.org/10.1016/j.frl.2021.102515

Ahmed, W. (2020). Stock market reactions to upside and downside volatility of bitcoin: a quantile analysis. North American Journal of Economics and Finance. (57). https://doi.org/10.1016/j.najef.2021.101379

Akinmade, B., Adedoyin, F.F., & Bekun, F.V. (2020). The impact of stock market manipulation on Nigerians economic performance. Journal of Economic Structures. https://doi.org/10.1186/s40008-020-00226-0

Antonakakis.N, Cunado.J, Filis.G, Gabauer.D, & Gracia.F.P (2020).Oil and asset classes implied volatilities: Investment strategies and hedging effectiveness. Energy Economics. (91). https://doi.org/10.1016/j.eneco.2020.104762

Baur, D. G., & McDermott, T. K. (2010). Is gold a safe haven? International evidence. Journal of Banking & Finance, 34(8), 1886–1898. https://doi.org/10.1016/j.jbankfin.2009.12.008

Bhuiyan, R.A., Husain, A. & Zhang, C. (2021). A wavelet approach for casual relationship between bitcoin and conventional asset classes. resource policy. (71). https://doi.org/10.1016/j.resourpol.2020.101971

Billmeier.A, (2014). Ghostbusting: Which output gap measure really matters. International Monetary Fund. 4(14). https://doi.org/10.5089/9781451856675.001

Bouri, E., Shahzad, S. J. H., Roubaud, D., Kristoufek, L., & Lucey, B. (2020). Bitcoin, gold, and commodities as safe-havens for stocks: New insight through wavelet analysis. The Quarterly Review of Economics and Finance, 77, 156–164. https://doi.org/10.1016/j.qref.2020.03.004

CBO, Congressional Budget Office (1995), CBO’s Method for Estimating Potential Output, CBO Memorandum, Washington, U.S. https://www.cbo.gov/publication/10603

Chigozie, O. & Nyatanga, P. (2020). An investigation into the crude oil pass- through to economic growth in Nigeria. Acta Universitatis Danubius Economica. 1(16). https://journals.univdanubius.ro/index.php/oeconomica/article/view/6432

Chijindu, A & Ifunanya, O. (2017). Stock market development and economic growth in Nigeria: a camaraderie reconnaissance. social science open access repository. 1-16. https://nbn-resolving.org/urn:nbn:de:0168-ssoar-56311-3

Chinyere, E.B., Chukwujekwu, O.P., Uchenna, A.W., & Chinedu, J. (2019). Response of stock market growth to fiscal policy in Nigeria: environmental impacts. international journal of applied environmental sciences.14(3).281-298. https://www.ripublication.com/ijaes19/ijaesv14n3_05.pdf

Chukwuka, E.A. & Nzotta, S.M. (2020). Effect of stock market on manufacturing sector output in Nigeria. International Journal of Management Sciences.8(3).53-61. https://arcnjournals.org/images/ASPL-IJMS-8-3-7.pdf

De Masi, P. (1997), IMF estimates of potential output: theory and practice, IMF working paper, 177, International Monetary Fund. 29, 1-16. https://econpapers.repec.org/paper/imfimfwpa/1997_2f177.html

Le, L., Yarovaya, L. & Nasir, M. (2021). Did covid-19 change spillover patterns between fintech and other asset classes? research in international business and finance. (58). https://doi.org/10.1016/j.ribaf.2021.101441

Ebun, F., Olusuyi, E. & Michael, A. (2018). The impact of stock market development on economic growth in Nigeria. Journal of Business and African Economy.4(1). https://iiardjournals.org/get/JBAE/VOL.%204%20NO.%201%202018/THE%20IMPACT%20OF%20STOCK.pdf

Efstathiou, K. (2019). The campaign against nonsense output gaps. bruegel. https://mishtalk.com/economics/the-campaign-against-nonsense-output-gaps/

Engle, R.F. (1982) “Autoregressive Conditional Heteroskedasticity with Estimates of The Variance of UK Inflation”, Econometrica 50, 987–1008. https://doi.org/0012-9682(198207)50:4<987:ACHWEO>2.0.CO;2-3

Ezenduka, V.G. & Joseph, E.M. (2020). Stock market performance and economic growth in Nigeria (1985-2018). international journal of accounting research. 5(4). https://doi.org/10.12816/0059066

Giorno, C., Richardson, P., Roseveare, D., & Van Den Noord, P. (1995), Estimating potential output, output gaps and structural budget balances, oecd economics department working paper No. 152, Paris. https://doi.org/10.1787/533876774515

Gudmundsson, T., Mrkaic, M., & Barkema, J. (2020). Output gaps in practice: proceed with caution. Cepr. https://cepr.org/voxeu/columns/output-gaps-practice-proceed-caution

Heiberger,H.R.(2018).Predicting economic growth with stock networks. physica a: statistical mechanics and its applications. (489). https://doi.org/10.1016/j.physa.2017.07.022

Henry.O, & Olabanji. O. (2013). Stock market performance and sustainable economic growth in Nigeria: bounds testing co-integration approach. journal of sustainable development .6(2). http://doi.org/10.5539/jsd.v6n8p84

Ishmael, O., Terry, M., & Park, I. (2017). The impact of changes in crude oil prices in economic growth in Nigeria: 1986-2015. Journal of Economics and Sustainable Development. 8(12).78-89. https://www.iiste.org/Journals/index.php/JEDS/article/view/37498

Majaski, C. (2021). Outputgap: What it means, pros and cons of using it. Investopedia. https://www.investopedia.com/terms/o/outputgap.asp

Meiryani, M., Delvin Tandyopranoto, C., Emanuel, J., Lindawati, A., Fahlevi, M., Aljuaid, M., Hasan, F., (2021) the effect of global price movements on the energy sector commodity on bitcoin price movement during the covid-19 pandemic, heliyon, https://doi.org/10.1016/j.heliyon.2022.e10820.

Mensi, W., Sensoy, A., Vo, X., & Kang, H. (2022). Pricing efficiency and asymmetric multifractality of major asset classes before and during covid-19 crisis. the north American journal of economics and finance. (62). https://doi.org/10.1016/j.najef.2022.101773

Michael, T., & Oyeyemi, M. (2018). Oil revenue and output growth in Nigeria. international journal of economics and business management.4(6). https://iiardjournals.org/abstract.php?j=IJEBM&pn=Oil%20Revenue%20and%20Output%20Growth%20in%20Nigeria&id=1548

Nweze, P., & Edame, E. (2016). An empirical investigation of oil revenue and economic growth in Nigeria. European Scientific Journal. 12(25). https://doi.org/10.19044/esj.2016.v12n25p271

• Ogunmuyiwa. M. (2010). Investors sentiment, stock market liquidity and economic growth in Nigeria. journal of social sciences.23(1). https://doi.org/10.1080/09718923.2010.11892812

Olabisi.P.O., Ejemeyovwi.O.J, Alege.O.P, Adu.O, & Ademola.O.A.(2017). Stock market and economic growth in Nigeria. International journal of English literature and social science.2(6). https://doi.org/10.24001/ijels.2.6.15

Olayongbo.D.(2019). Effects of oil export revenue on economic growth in Nigeria: a time varying analysis of resource course. Resources Policy.64. https://doi.org/10.1016/j.resourpol.2019.101469

Omitogun.O, Longe.E., & Muhammed.S (2018). The impact of oil price and revenue variation on economic growth in Nigeria. opec energy review. 42(4). 387-402. https://doi.org/10.1111/opec.12139

Paul, A. O & Mmeyene-Abasi, E.A. (2022). Gold demand determinants and reserve building capacity of the Nigerian economy: inputs from a panel analysis of selected countries, journal of world economic research.11(1), pp. 27-44. https://doi.org/10.11648/j.jwer.20221101.14

Pedro.I & Adesina-Uthman.G.A.(2022). Impact of Monetary Policy Shocks on the Output Gap in Nigeria. International Journal of Economics.14(9). https://doi.org/10.5539/ijef.v14n9p38

Pham, L., & Nguyen, C.P. (2021). Asymmetric tail dependence between green bonds and other asset classes. Global Finance Journal. 50. https://doi.org/10.1016/j.gfj.2021.100669

Reboredo, J. C. (2013). Is gold a hedge or safe haven against oil price movements? Resources Policy, 38(2), 130–137. https://doi.org/10.1016/j.resourpol.2013.02.003

Satti, A. U. H., & Malik, W. S. (2017). The Unreliability of Output-Gap Estimates in Real Time. The PakistanDevelopment Review, 56(3), 193-219. https://doi.org/10.30541/v56i3pp.193-219 (1) (PDF) Impact of Monetary Policy Shocks on the Output Gap in Nigeria. Available from: https://www.jstor.org/stable/44986415

Shahzad, S. J. H., Bouri, E., Roubaud, D., Kristoufek, L., & Lucey, B. (2019). Is Bitcoin a better safe-haven investment than gold and commodities? International Review of Financial Analysis, 63, 322–330. https://doi.org/10.1016/j.irfa.2019.01.002

Yousaf, I., Bouri, E., Ali, S., & Azoury, N. (2021). Gold against Asian Stock Markets during the COVID-19 Outbreak. Journal of Risk and Financial Management, 14(4), 186. https://doi.org/10.3390/jrfm14040186

Yousaf, I., Pham, L., & Goodell, J. (2023). The connectedness between meme tokens, meme stocks, and other asset classes: evidence from a quantile connectedness approach. Journal of international financial markets, institutions and money. (82). https://doi.org/10.1016/j.intfin.2022.101694