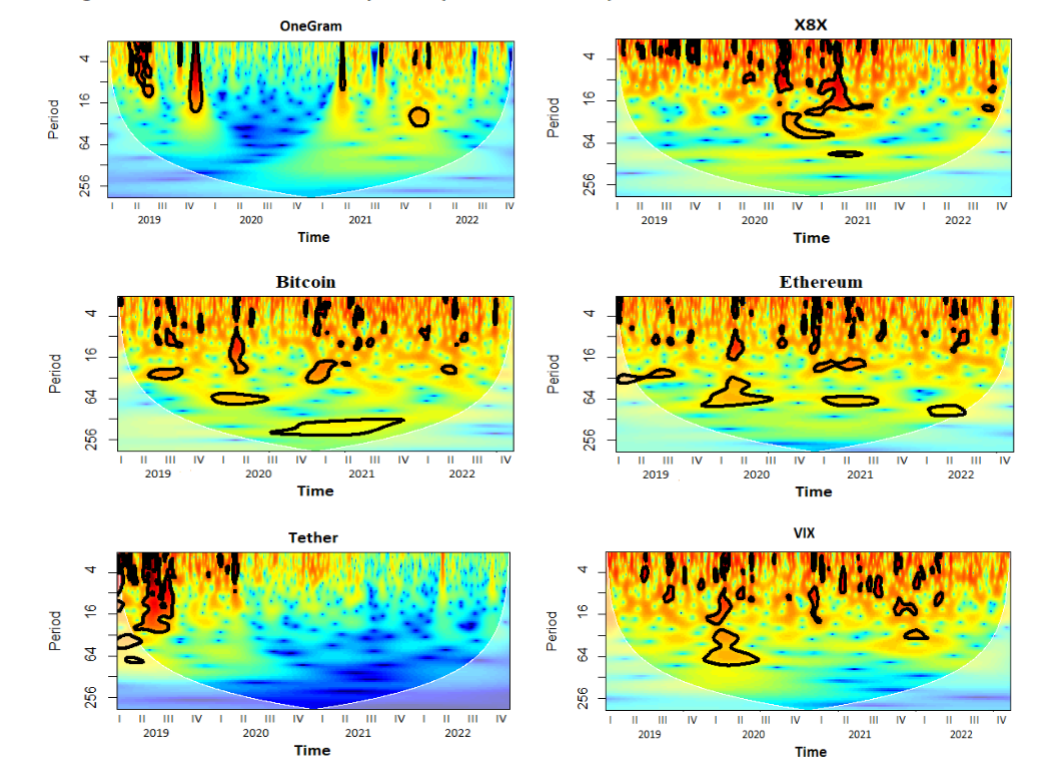

We extend the Shariah-compliant digital assets and Islamic Fintech literature through exploring the time-frequency associations between the volatility index (VIX) and cryptocurrencies (both Islamic and traditional). Employing wavelet-based technique, we find that Islamic cryptocurrencies demonstrate low or no coherency with stock market volatility compared to traditional cryptocurrencies (except Tether) during the whole time and frequency bands, highlighting the hedging capabilities of Islamic cryptocurrencies. Tether also serves the same against VIX, as there is a low or favorable link between these variables. Finally, our findings would be prolific to digital currency traders and investors in designing the portfolio strategies.

Rashid, M. M., & Amin, M. R. (2023). Time-frequency dependency between stock market volatility, and Islamic gold-backed and conventional cryptocurrencies. Financial Economics Letters, 2(1), 6. doi:10.58567/fel02010001

ACS Style

Rashid, M. M.; Amin, M. R. Time-frequency dependency between stock market volatility, and Islamic gold-backed and conventional cryptocurrencies. Financial Economics Letters, 2023, 2, 6. doi:10.58567/fel02010001

AMA Style

Rashid M M, Amin M R. Time-frequency dependency between stock market volatility, and Islamic gold-backed and conventional cryptocurrencies. Financial Economics Letters; 2023, 2(1):6. doi:10.58567/fel02010001

Chicago/Turabian Style

Rashid, Md. M.; Amin, Md. R. 2023. "Time-frequency dependency between stock market volatility, and Islamic gold-backed and conventional cryptocurrencies" Financial Economics Letters 2, no.1:6. doi:10.58567/fel02010001

Rashid, M. M.; Amin, M. R. Time-frequency dependency between stock market volatility, and Islamic gold-backed and conventional cryptocurrencies. Financial Economics Letters, 2023, 2, 6. doi:10.58567/fel02010001

AMA Style

Rashid M M, Amin M R. Time-frequency dependency between stock market volatility, and Islamic gold-backed and conventional cryptocurrencies. Financial Economics Letters; 2023, 2(1):6. doi:10.58567/fel02010001

Chicago/Turabian Style

Rashid, Md. M.; Amin, Md. R. 2023. "Time-frequency dependency between stock market volatility, and Islamic gold-backed and conventional cryptocurrencies" Financial Economics Letters 2, no.1:6. doi:10.58567/fel02010001

APA style

Rashid, M. M., & Amin, M. R. (2023). Time-frequency dependency between stock market volatility, and Islamic gold-backed and conventional cryptocurrencies. Financial Economics Letters, 2(1), 6. doi:10.58567/fel02010001

Article Metrics

Article Access Statistics

References

Akhtar, S., & Jahromi, M. (2017). Impact of the global financial crisis on Islamic and conventional stocks and bonds. Accounting & Finance, 57(3), 623-655. https://doi.org/10.1111/acfi.12136

Ali, F., Bouri, E., Naifar, N., Shahzad, S. J. H., & AlAhmad, M. (2022). An examination of whether gold-backed Islamic cryptocurrencies are safe havens for international Islamic equity markets. Research in International Business and Finance, 63, 101768. https://doi.org/10.1016/j.ribaf.2022.101768

Aloui, C., ben Hamida, H., & Yarovaya, L. (2021). Are Islamic gold-backed cryptocurrencies different? Finance Research Letters, 39, 101615. https://doi.org/10.1016/j.frl.2020.101615

Al-Yahyaee, K. H., Mensi, W., Rehman, M. U., Vo, X. V., & Kang, S. H. (2020). Do Islamic stocks outperform conventional stock sectors during normal and crisis periods? Extreme co-movements and portfolio management analysis. Pacific-Basin Finance Journal, 62, 101385. https://doi.org/10.1016/j.pacfin.2020.101385

Baur, D. G., & Hoang, L. T. (2021). A crypto safe haven against Bitcoin. Finance Research Letters, 38, 101431. https://doi.org/10.1016/j.frl.2020.101431

Baur, D. G., Hong, K., & Lee, A. D. (2018). Bitcoin: Medium of exchange or speculative assets? Journal of International Financial Markets, Institutions and Money, 54, 177–189. https://doi.org/10.1016/j.intfin.2017.12.004

Bouri, E., Shahzad, S. J. H., Roubaud, D., Kristoufek, L., & Lucey, B. (2020). Bitcoin, gold, and commodities as safe havens for stocks: New insight through wavelet analysis. The Quarterly Review of Economics and Finance, 77, 156-164. https://doi.org/10.1016/j.qref.2020.03.004

Conlon, T., & McGee, R. (2020). Safe haven or risky hazard? Bitcoin during the COVID-19 bear market. Finance Research Letters, 35, 101607. https://doi.org/10.1016/j.frl.2020.101607

Hasan, M. B., Hassan, M. K., Gider, Z., Rafia, H. T., & Rashid, M. (2023). Searching Hedging Instruments Against Diverse Global Risks and Uncertainties. The North American Journal of Economics and Finance 66, 101893. https://doi.org/10.1016/j.najef.2023.101893

Hasan, M. B., Hassan, M. K., Rashid, M. M., & Alhenawi, Y. (2021). Are safe haven assets really safe during the 2008 global financial crisis and COVID-19 pandemic? Global Finance Journal, 50, 100668. https://doi.org/10.1016/j.gfj.2021.100668

Hasan, M. B., Rashid, M. M., Shafiullah, M., & Sarker, T. (2022). How resilient are Islamic financial markets during the COVID-19 pandemic? Pacific-Basin Finance Journal, 74, 101817. https://doi.org/10.1016/j.pacfin.2022.101817

Hassan, M. K., Hasan, M. B., Halim, Z. A., Maroney, N., & Rashid, M. M. (2022). Exploring the dynamic spillover of cryptocurrency environmental attention across the commodities, green bonds, and environment-related stocks. The North American Journal of Economics and Finance, 61, 101700. https://doi.org/10.1016/j.najef.2022.101700

Jiang, Y., Nie, H., & Ruan, W. (2018). Time-varying long-term memory in Bitcoin market. Finance Research Letters, 25, 280-284. https://doi.org/10.1016/j.frl.2017.12.009

Mnif, E., Salhi, B., Trabelsi, L., & Jarboui, A. (2022). Efficiency and herding analysis in gold-backed cryptocurrencies. Heliyon, 8(12), e11982. https://doi.org/10.1016/j.heliyon.2022.e11982

Mo, B., Meng, J., & Zheng, L. (2022). Time and frequency dynamics of connectedness between cryptocurrencies and commodity markets. Resources Policy, 77, 102731. https://doi.org/10.1016/j.resourpol.2022.102731

Nadarajah, S., & Chu, J. (2017). On the inefficiency of Bitcoin. Economics Letters, 150, 6–9. https://doi.org/10.1016/j.econlet.2016.09.019

Shahzad, S. J. H., Bouri, E., Ahmad, T., & Naeem, M. A. (2022). Extreme tail network analysis of cryptocurrencies and trading strategies. Finance Research Letters, 44, 102106. https://doi.org/10.1016/j.frl.2021.102106

Torrence, C., & Compo, G. P. (1998). A practical guide to wavelet analysis. Bulletin of the American Meteorological Society, 79(1), 61-78. https://doi.org/10.1175/1520-0477(1998)079<0061:APGTWA>2.0.CO;2

Torrence, C., & Webster, P. J. (1998). The annual cycle of persistence in the El Nino/Southern Oscillation. Quarterly Journal of the Royal Meteorological Society, 124(550), 1985-2004. https://doi.org/10.1002/qj.49712455010

Umar, Z., Gubareva, M., & Teplova, T. (2021). The impact of Covid-19 on commodity markets volatility: Analyzing time-frequency relations between commodity prices and coronavirus panic levels. Resources Policy, 73, 102164. https://doi.org/10.1016/j.resourpol.2021.102164

Urquhart, A. (2016). The inefficiency of Bitcoin. Economics Letters, 148, 80–82. https://doi.org/10.1016/j.econlet.2016.09.019

Yousaf, I., & Yarovaya, L. (2022). Spillovers between the Islamic gold-backed cryptocurrencies and equity markets during the COVID-19: A sectorial analysis. Pacific-Basin Finance Journal, 71, 101705. https://doi.org/10.1016/j.pacfin.2021.101705