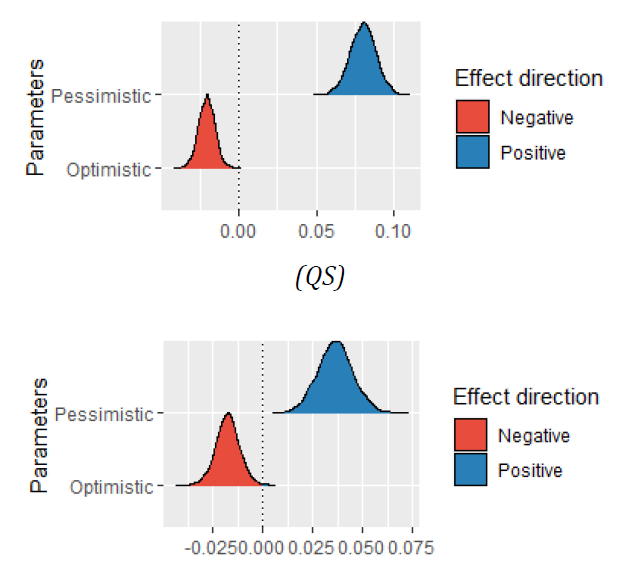

The current study examines the performance of 76 Japanese equity Exchange Traded Funds (ETFs) over the period 1/1/2018-12/31/2022. Performance is estimated in several ways, that is, raw returns, alphas from single- and multi-factor regression models, and risk-adjusted returns. The market timing skills of ETF managers are examined too. The results reveal that, on average, the examined ETFs do not produce any material alpha. The results also indicate that the risk factors suggested by Fama and French (1993 & 2015) are more or less capable of explaining the performance of the Japanese ETFs. Finally, the findings show that 21% of ETF managers possess some sort of market timing skills. However, the managers fail to time the volatility of the stock market.

Rompotis, G. G. (2024). A Study on the Performance of Japanese ETFs. Economic Analysis Letters, 3(3), 64. doi:10.58567/eal03030005

ACS Style

Rompotis, G. G. A Study on the Performance of Japanese ETFs. Economic Analysis Letters, 2024, 3, 64. doi:10.58567/eal03030005

AMA Style

Rompotis G G. A Study on the Performance of Japanese ETFs. Economic Analysis Letters; 2024, 3(3):64. doi:10.58567/eal03030005

Chicago/Turabian Style

Rompotis, Gerasimos G. 2024. "A Study on the Performance of Japanese ETFs" Economic Analysis Letters 3, no.3:64. doi:10.58567/eal03030005

Share and Cite

ACS Style

Rompotis, G. G. A Study on the Performance of Japanese ETFs. Economic Analysis Letters, 2024, 3, 64. doi:10.58567/eal03030005

AMA Style

Rompotis G G. A Study on the Performance of Japanese ETFs. Economic Analysis Letters; 2024, 3(3):64. doi:10.58567/eal03030005

Chicago/Turabian Style

Rompotis, Gerasimos G. 2024. "A Study on the Performance of Japanese ETFs" Economic Analysis Letters 3, no.3:64. doi:10.58567/eal03030005

APA style

Rompotis, G. G. (2024). A Study on the Performance of Japanese ETFs. Economic Analysis Letters, 3(3), 64. doi:10.58567/eal03030005

Article Metrics

Article Access Statistics

References

Adachi, K., Hiraki, K., and Kitamura, T. (2021). The Effects of the Bank of Japan’s ETF Purchases on Risk Premia in the Stock Markets. Working Paper, Bank of Japan.

Barbon, A., and Gianinazzi, V. (2019). Quantitative Easing and Equity Prices: Evidence from the ETF Program of the Bank of Japan. Review of Asset Pricing Studies 9(2), 210-255. https://doi.org/10.1093/rapstu/raz008

Carhart, M. (1997). On Persistence in Mutual Fund Performance. Journal of Finance 52(1), 57-82. https://doi.org/10.2307/2329556

Charoenwong, B., Morck, R., and Wiwattanakantang, Y. (2021) Bank of Japan Equity Purchases: The (Non-)Effects of Extreme Quantitative Easing. Review of Finance 25(3), 713-743. https://doi.org/10.1093/rof/rfaa029

Fama, E.F., and French, K.R. (1993). Common Risk Factors in the Returns on Stocks and Bonds. Journal of Financial Economics 33, 3-56. https://doi.org/10.1016/0304-405X(93)90023-5

Fama, E.F., and French, K.R. (2015) A Five-Factor Asset Pricing Model. Journal of Financial Economics 116, 1-22. https://doi.org/10.1016/j.jfineco.2014.10.010

Gunji, H., Miura, K., and Yuan, Y. (2021). The Effect of the Bank of Japan’s ETF Purchases on Firm Performance. Working Paper

Hanaeda, H., and Serita, T. (2017). Effects of Nikkei 225 ETFs on Stock Markets: Impacts of Purchases by Bank of Japan. 30th Australasian Finance and Banking Conference 2017, 13-15 December 2017, Sydney.

Harada, K., and Okimoto, T. (2021). The BOJ’s ETF Purchases and Its Effects on Nikkei 225 Stocks. International Review of Financial Analysis 77, 1-11. https://doi.org/10.1016/j.irfa.2021.101826

Hattori, T., and Yoshida, J. (2023). The Impact of Bank of Japan’s Exchange-Traded Fund Purchases. Journal of Financial Stability 65. https://doi.org/10.1016/j.jfs.2023.101102

Holmes, K.A., and Faff, R.W. (2004). Stability, Asymmetry and Seasonality of Fund Performance: An Analysis of Australian Multi-sector Managed Funds. Journal of Business Finance & Accounting 31(3-4), 539-578. https://doi.org/10.1111/j.0306-686X.2004.00549.x

Iwai, K. (2009). Wagakuni ETF Sizyo no Maaketto Maikuro Sutorakucha to Tousika no Chuumon Koudou (Market Microstructure of Japanese ETF Market and Investors Behavior. FSA Research Review 5, 5-53, (in Japanese).

Iwai, K. (2010). Nihon no ETF Sizyo niokeru Hikouritsusei to Sono Hassei Genin (Inefficiency in the Japanese ETF Market). FSA Discussion Paper Series, DP2010-5, (in Japanese).

Iwai, K. (2011) Why Does the Law of One Price Fail in Japanese ETF Markets? FSA Discussion Paper Series, DP2011-3.

Jagannathan, R., and Korajczyk, R.A. (1986). Assessing the Market Timing Performance of Managed Portfolios. Journal of Business 59(2), 217-235. https://www.jstor.org/stable/2353018

Katagiri, M., Takahashi, K., and Shino, J. (2022) Bank of Japan’s ETF Purchase Program and Equity Risk Premium: A CAPM Interpretation. Working Paper, Bank for International Settlements.

Kono, PD., Yatrakis, P., and Segal, S. (2011). An Empirical Study of Japanese Market Efficiency: Comparing The Risk-Adjusted Performance Of An ETF Portfolio Versus The Topix Index. Global Journal of Management and Business Research 11(5), 1-4.

Koyama, K. (2020). The Bank of Japan’s Equity Exchange-Traded Funds Purchasing Operation and its Impact on Equity Returns. Cogent Economics and Finance 10(1), 1-20. https://doi.org/10.1080/23322039.2022.2111782

Miu, P., Yueh, M.-L., and Han, J. (2021). Performance of Japanese Leveraged ETFs. Pacific-Basin Finance Journal 65, 101490. https://doi.org/10.1016/j.pacfin.2020.101490

Rompotis, G.G. (2013). Actively vs. Passively Managed Exchange Traded Funds. The IEB International Journal of Finance 6, 116-135.

Treynor, J., and Mazuy, K. (1966). Can Mutual Funds Outguess the Market? Harvard Business Review 44(4), 131-136.