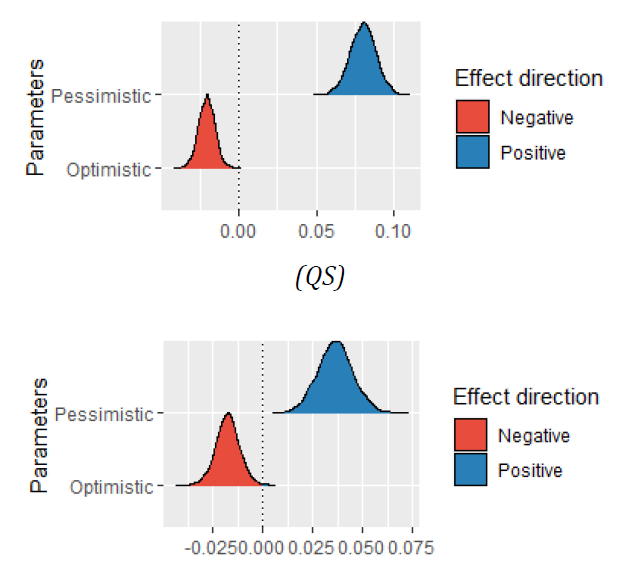

This paper specifically underscores the disparities among various ESG rating systems in China, highlighting their varied interpretations and emphasis on corporate financial factors. Analyzing data on Chinese listed firms from 2009-2022, we observe that while company size and leverage ratio uniformly correlate with ESG scores across rating agencies such as Bloomberg, Huazheng, Wind, and Hexun, the influence of factors like return on assets, cash flow, company age, and Tobin's Q is markedly inconsistent among these agencies. For instance, while operational cash flow and company age are positively associated with ESG ratings from Bloomberg, Huazheng, and Wind, they hold an inverse relationship with Hexun's ratings. This divergence underscores the unique data collection, weighting, and evaluation methodologies employed by each rating system. The study emphasizes the criticality of comprehending the nuances of each rating agency's approach when interpreting ESG scores and crafting ESG strategies. Moreover, it advocates for integrating insights from multiple rating systems to cater to the diverse expectations of stakeholders.

Zhu, C., & Yang, C. (2024). Divergences among ESG rating systems: Evidence from financial indexes. Economic Analysis Letters, 3(1), 48. doi:10.58567/eal03010006

ACS Style

Zhu, C.; Yang, C. Divergences among ESG rating systems: Evidence from financial indexes. Economic Analysis Letters, 2024, 3, 48. doi:10.58567/eal03010006

AMA Style

Zhu C, Yang C. Divergences among ESG rating systems: Evidence from financial indexes. Economic Analysis Letters; 2024, 3(1):48. doi:10.58567/eal03010006

Chicago/Turabian Style

Zhu, Conghao; Yang, Cunyi 2024. "Divergences among ESG rating systems: Evidence from financial indexes" Economic Analysis Letters 3, no.1:48. doi:10.58567/eal03010006

Funding

National Natural Science Foundation of China (72371256)

,

the Excellent Young Team Project Natural Science Foundation of Guangdong Province of China (2023B1515040001)

,

Tianjin Foreign Studies University (2022YJ5092)

Share and Cite

ACS Style

Zhu, C.; Yang, C. Divergences among ESG rating systems: Evidence from financial indexes. Economic Analysis Letters, 2024, 3, 48. doi:10.58567/eal03010006

AMA Style

Zhu C, Yang C. Divergences among ESG rating systems: Evidence from financial indexes. Economic Analysis Letters; 2024, 3(1):48. doi:10.58567/eal03010006

Chicago/Turabian Style

Zhu, Conghao; Yang, Cunyi 2024. "Divergences among ESG rating systems: Evidence from financial indexes" Economic Analysis Letters 3, no.1:48. doi:10.58567/eal03010006

APA style

Zhu, C., & Yang, C. (2024). Divergences among ESG rating systems: Evidence from financial indexes. Economic Analysis Letters, 3(1), 48. doi:10.58567/eal03010006

Article Metrics

Article Access Statistics

References

Adams, C. A., W.-Y. Hill, and C. B. Roberts. (1998). Corporate social reporting practices in Western Europe: legitimating corporate behaviour? The British accounting review 30 (1):1-21. https://doi.org/10.1006/bare.1997.0060

Baldini, M., L. D. Maso, G. Liberatore, F. Mazzi, and S. Terzani. (2018). Role of country-and firm-level determinants in environmental, social, and governance disclosure. Journal of business ethics 150:79-98. https://doi.org/10.1007/s10551-016-3139-1

Benlemlih, M., and I. Girerd‐Potin. (2017). Corporate social responsibility and firm financial risk reduction: On the moderating role of the legal environment. Journal of Business Finance & Accounting 44 (7-8):1137-1166. https://doi.org/10.1111/jbfa.12251

Gallo, P. J., and L. J. Christensen. (2011). Firm size matters: An empirical investigation of organizational size and ownership on sustainability-related behaviors. Business & Society 50 (2):315-349. https://doi.org/10.1177/0007650311398784

Gangi, F., and E. D’Angelo. (2016). The virtuous circle of corporate social performance and corporate social disclosure. Modern Economy 7 (12):1396. https://doi.org/10.4236/me.2016.712129

Graafland, J., B. Van de Ven, and N. Stoffele. (2003). Strategies and instruments for organising CSR by small and large businesses in the Netherlands. Journal of business ethics 47:45-60. https://doi.org/10.1023/A:1026240912016

Hörisch, J., M. P. Johnson, and S. Schaltegger. (2015). Implementation of sustainability management and company size: A knowledge‐based view. Business Strategy and the Environment 24 (8):765-779. https://doi.org/10.1002/bse.1844

Li, W., and W. Pang. (2023). The impact of digital inclusive finance on corporate ESG performance: based on the perspective of corporate green technology innovation. Environmental Science and Pollution Research 30 (24):65314-65327. https://doi.org/10.1007/s11356-023-27057-3

Udayasankar, K. (2008). Corporate social responsibility and firm size. Journal of business ethics 83 (2):167-175. https://doi.org/10.1007/s10551-007-9609-8

Zhai, Y., Z. Cai, H. Lin, M. Yuan, Y. Mao, and M. Yu. (2022). Does better environmental, social, and governance induce better corporate green innovation: The mediating role of financing constraints. Corporate Social Responsibility and Environmental Management 29 (5):1513-1526. https://doi.org/10.1002/csr.2288