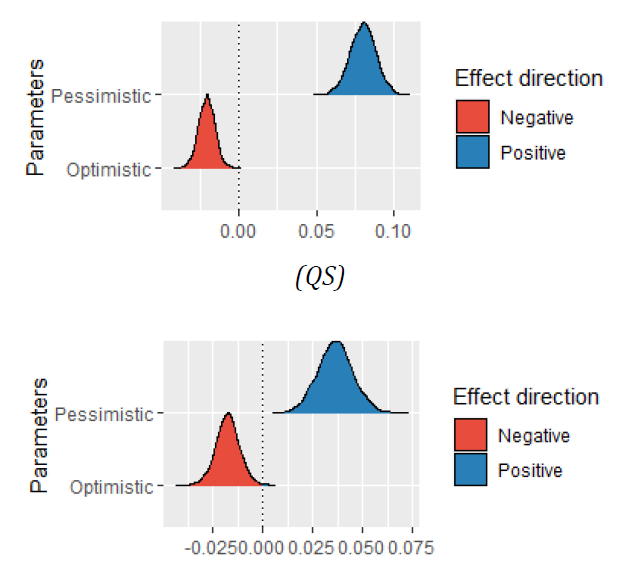

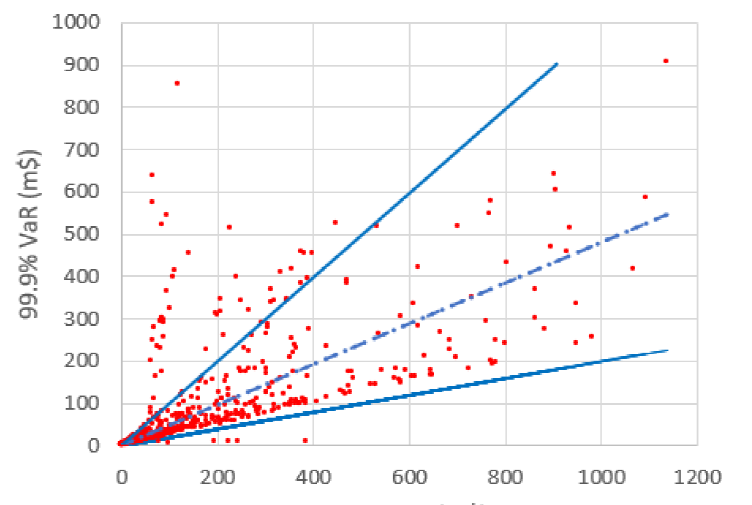

Calculating the amount of regulatory capital to cover unexpected losses due to operational events in the upcoming year has caused problems because of difficulties in fitting probability distributions to data. It is consequently difficult to judge an appropriate level of capital that reflects the risk profile of a financial institution. We provide theoretical and empirical analyses to link the calculated capital to the sum of losses using appropriate statistical approximations. We conclude that, in order to reasonably reflect the associated risk, the capital should be approximately half the sum of losses, with a wide bound for the ratio of capital to sum.

Mitic, P. Reasonableness and Correctness for Operational Value-at-Risk. Economic Analysis Letters, 2023, 2, 31. doi:10.58567/eal02030005

AMA Style

Mitic P.. Reasonableness and Correctness for Operational Value-at-Risk. Economic Analysis Letters; 2023, 2(3):31. doi:10.58567/eal02030005

Chicago/Turabian Style

Mitic, Peter 2023. "Reasonableness and Correctness for Operational Value-at-Risk" Economic Analysis Letters 2, no.3:31. doi:10.58567/eal02030005

APA style

Mitic, P. (2023). Reasonableness and Correctness for Operational Value-at-Risk. Economic Analysis Letters, 2(3), 31. doi:10.58567/eal02030005

Article Metrics

Article Access Statistics

References

Abdymomunov, A. and Curti, F. (2020). Quantifying and stress testing operational risk with peer banks’ data. Journal of Financial Services Research, 57, 287-313. https://doi.org/10.1007/s10693-019-00320-w

Abdymomunov, A., Curti, F., and Mihov, A. (2020). U.S. banking sector operational losses and the macroeconomic environment. Journal of Money, Credit, and Banking, 52(1), 115–144. https://doi.org/10.1111/jmcb.12661

Berkowitz, J. and O’Brian, J. (2002). How accurate are value-at-risk models at commercial banks? Journal of Finance, 57(3), 1093–1111. https://doi.org/10.1111/1540-6261.00455

BIS (2006). Bank for International Settlements BCBS128 - International Convergence of Capital Measurement and Capital Standards. https://www.bis.org/publ/bcbs128.htm

Chen,Q. and Wen,Y. (2010). A BP-Neural Network Predictor Model for Operational Risk Losses of Commercial Bank. 3rd Int. Symposium on Information Processing, Qingdao, 291-295. https://doi.org/10.1109/ISIP.2010.43

Efron, B and Tibshirani, R.J. (1994) An Introduction to the Bootstrap, Chapman Hall

Frachot, A., Georges, P., and Roncalli, T. (2001). Loss distribution approach for operational risk. Working paper, Groupe de Recherche Operationnelle, Credit Lyonnais, France. http://ssrn.com/abstract=1032523

Mitic, P., Cooper, J. and Bloxham, N. (2020). Incremental Value-at-Risk. Journal of Model Risk Validation, 14(1), 1-37. https://doi.org/10.21314/JRMV.2020.216

Mitic, P. (2015). Improved Goodness-of-Fit tests for Operational Risk. Journal of Operational Risk, 15(1), 77-126. https://doi.org/10.21314/JOP.2015.159

Mitic, P. (2023). Credible Value-at-Risk. Submitted to the Journal of Operational Risk

Pena,A., Patino, A., Chiclana, F., Caraffini, F. and Congora, M. (2021). Fuzzy convolutional deep-learning model to estimate the operational risk capital using multi-source risk events. Applied Soft Computing 107(107381). https://www.sciencedirect.com/science/article/pii/S1568494621003045

Stuart, R. (2023) Why did Credit Suisse fail? Economics Observatory https://www.economicsobservatory.com/

Weisstein, E. W. (2023) Wolfram MathWorld. https://mathworld.wolfram.com