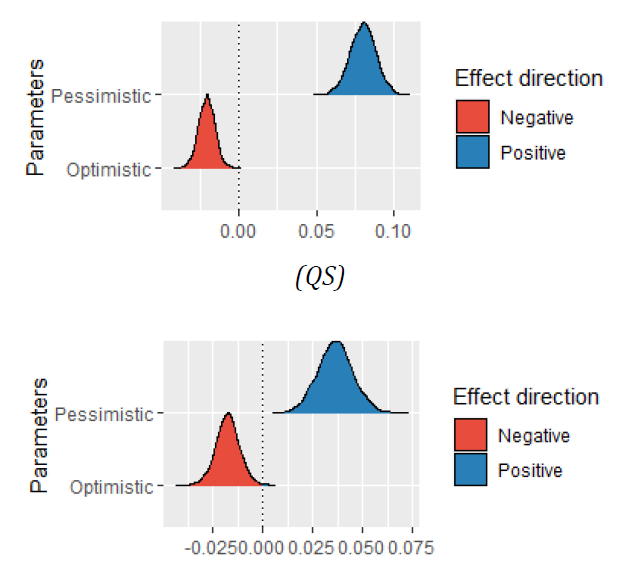

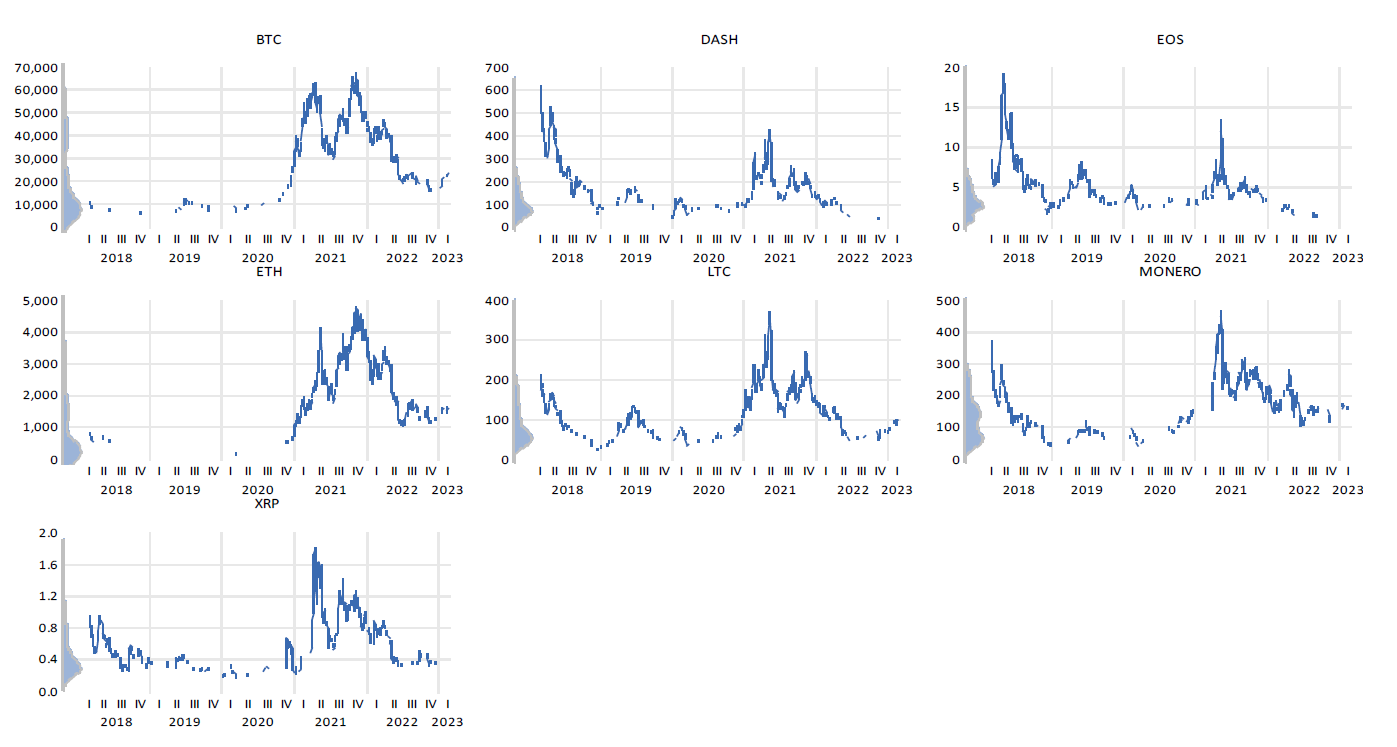

In this study, we examined the efficiency of cryptocurrencies Bitcoin (BTC), Ethereum (ETH), Litecoin (LTC), Ripple (XRP), DASH, EOS, and MONERO from March 1, 2018, to March 1, 2023. We separated the sample into four subperiods for this purpose: a Tranquil period that includes the period from March 1, 2018, to December 31, 2019; a First Wave that includes the year 2020; a Second Wave that includes the year 2021; and a fourth subperiod that includes Russia's invasion of Ukraine in 2022-2023. The results are mixed, with some cryptocurrencies exhibiting equilibrium and others exhibiting autocorrelation and predictability in their pricing. When the sample is divided into subperiods, most digital currencies have long memories in their returns during the Tranquil period, BTC, LTC, and XRP exhibit efficiency during the First Wave of the pandemic, while BTC, ETH, and MONERO indicate efficiency during the Second Wave. Most assessed digital currencies showed equilibrium by 2022, with the exception of ETH and MONERO, which exhibit long memories, and LTC, which demonstrates anti-persistence. These results hold significance for investors in these alternative markets, as they suggest that some cryptocurrencies may be more predictable and therefore potentially profitable, whereas others may require greater caution and risk management strategies.

Chambino, M., Dias, R. M. T., & Horta, N. R. (2023). Asymmetric efficiency of cryptocurrencies during the 2020 and 2022 events. Economic Analysis Letters, 2(2), 22. doi:10.58567/eal02020004

ACS Style

Chambino, M.; Dias, R. M. T.; Horta, N. R. Asymmetric efficiency of cryptocurrencies during the 2020 and 2022 events. Economic Analysis Letters, 2023, 2, 22. doi:10.58567/eal02020004

AMA Style

Chambino M, Dias R M T, Horta N R. Asymmetric efficiency of cryptocurrencies during the 2020 and 2022 events. Economic Analysis Letters; 2023, 2(2):22. doi:10.58567/eal02020004

Chicago/Turabian Style

Chambino, Mariana; Dias, Rui M. T.; Horta, Nicole R. 2023. "Asymmetric efficiency of cryptocurrencies during the 2020 and 2022 events" Economic Analysis Letters 2, no.2:22. doi:10.58567/eal02020004

Chambino, M.; Dias, R. M. T.; Horta, N. R. Asymmetric efficiency of cryptocurrencies during the 2020 and 2022 events. Economic Analysis Letters, 2023, 2, 22. doi:10.58567/eal02020004

AMA Style

Chambino M, Dias R M T, Horta N R. Asymmetric efficiency of cryptocurrencies during the 2020 and 2022 events. Economic Analysis Letters; 2023, 2(2):22. doi:10.58567/eal02020004

Chicago/Turabian Style

Chambino, Mariana; Dias, Rui M. T.; Horta, Nicole R. 2023. "Asymmetric efficiency of cryptocurrencies during the 2020 and 2022 events" Economic Analysis Letters 2, no.2:22. doi:10.58567/eal02020004

APA style

Chambino, M., Dias, R. M. T., & Horta, N. R. (2023). Asymmetric efficiency of cryptocurrencies during the 2020 and 2022 events. Economic Analysis Letters, 2(2), 22. doi:10.58567/eal02020004

Article Metrics

Article Access Statistics

References

Chu, J., Zhang, Y., & Chan, S. (2019a). The adaptive market hypothesis in the high frequency cryptocurrency market. International Review of Financial Analysis, 64, 221–231. https://doi.org/10.1016/J.IRFA.2019.05.008

Chu, J., Zhang, Y., & Chan, S. (2019b). The adaptive market hypothesis in the high frequency cryptocurrency market. International Review of Financial Analysis, 64, 221–231. https://doi.org/10.1016/J.IRFA.2019.05.008

Dias, R., & Carvalho, L. C. (2020). Hedges and safe havens: An examination of stocks, gold and silver in Latin America’s stock market. Revista de Administração Da UFSM, 13(5), 1114–1132. https://doi.org/10.5902/1983465961307

Dias, R., Heliodoro, P., Teixeira, N., & Godinho, T. (2020). Testing the Weak Form of Efficient Market Hypothesis: Empirical Evidence from Equity Markets. International Journal of Accounting, Finance and Risk Management, 5(1). https://doi.org/10.11648/j.ijafrm.20200501.14

Dias, R., Pardal, P., Teixeira, N., & Horta, N. (2022). Tail Risk and Return Predictability for Europe’ s Capital Markets : An Approach in Periods of the. December. https://doi.org/10.4018/978-1-6684-5666-8.ch015

Dias, R., & Santos, H. (2020a). Stock Market Efficiency in Africa: Evidence from Random Walk Hypothesis. 6th LIMEN Conference Proceedings (Part of LIMEN Conference Collection), 6(July), 25–37. https://doi.org/10.31410/limen.2020.25

Dias, R., & Santos, H. (2020b). the Impact of Covid-19 on Exchange Rate Volatility: an Econophysics Approach. 6th LIMEN Conference Proceedings (Part of LIMEN Conference Collection), 6(July), 39–49. https://doi.org/10.31410/limen.2020.39

Dias, R. T., Pardal, P., Santos, H., & Vasco, C. (2021). Testing the Random Walk Hypothesis for Real Exchange Rates (Issue June, pp. 304–322). https://doi.org/10.4018/978-1-7998-6926-9.ch017

Dickey, D., & Fuller, W. (1981). Likelihood ratio statistics for autoregressive time series with a unit root. Econometrica, 49(4), 1057–1072. https://doi.org/10.2307/1912517

Drożdż, S., Gȩbarowski, R., Minati, L., Oświȩcimka, P., & Wa̧torek, M. (2018a). Bitcoin market route to maturity? Evidence from return fluctuations, temporal correlations and multiscaling effects. Chaos, 28(7). https://doi.org/10.1063/1.5036517

Drożdż, S., Gȩbarowski, R., Minati, L., Oświȩcimka, P., & Wa̧torek, M. (2018b). Bitcoin market route to maturity? Evidence from return fluctuations, temporal correlations and multiscaling effects. Chaos, 28(7). https://doi.org/10.1063/1.5036517

Fama, E. F. (1970). Efficient Capital Markets: A Review of Theory and Empirical Work. The Journal of Finance. https://doi.org/10.2307/2325486

Fama, E. F. (1991). Efficient Capital Markets: II. The Journal of Finance. https://doi.org/10.2307/2328565

Guedes, E. F., Santos, R. P. C., Figueredo, L. H. R., Da Silva, P. A., Dias, R. M. T. S., & Zebende, G. F. (2022). Efficiency and Long-Range Correlation in G-20 Stock Indexes: A Sliding Windows Approach. Fluctuation and Noise Letters. https://doi.org/10.1142/S021947752250033X

Horta, N., Dias, R., Revez, C., & Alexandre, P. (2022). Cryptocurrencies and G7 capital markets integrate in periods of extreme volatility? Journal of process management and new technologies 10(3), 121–130.

Im, K. S., Pesaran, M. H., & Shin, Y. (2003). Testing for unit roots in heterogeneous panels. Journal of Econometrics. https://doi.org/10.1016/S0304-4076(03)00092-7

Jarque, C. M., & Bera, A. K. (1980). Efficient tests for normality, homoscedasticity and serial independence of regression residuals. Economics Letters, 6(3). https://doi.org/10.1016/0165-1765(80)90024-5

Kristoufek, L. (2018). On Bitcoin markets (in)efficiency and its evolution. Physica A: Statistical Mechanics and Its Applications, 503, 257–262. https://doi.org/10.1016/J.PHYSA.2018.02.161

Levin, A., Lin, C. F., & Chu, C. S. J. (2002). Unit root tests in panel data: Asymptotic and finite-sample properties. Journal of Econometrics, 108(1). https://doi.org/10.1016/S0304-4076(01)00098-7

Lo, A. W., & MacKinlay, A. C. (1988). Stock Market Prices Do Not Follow Random Walks: Evidence from a Simple Specification Test. Review of Financial Studies, 1(1). https://doi.org/10.1093/rfs/1.1.41

Pardal, P., Dias, R., Teixeira, N. & Horta, N. (2022). The Effects of Russia’ s 2022 Invasion of Ukraine on Global Markets : An Analysis of Particular Capital and Foreign Exchange Markets. Handbook of Research on Acceleration Programs for SMEs. https://doi.org/10.4018/978-1-6684-5666-8.ch014

Phillips, P. C. B., & Perron, P. (1988). Testing for a unit root in time series regression. Biometrika, 75(2), 335–346. https://doi.org/10.1093/biomet/75.2.335

Revez, C., Dias, R., Horta, N., Heliodoro, P., & Alexandre, P. (2022). Capital Market Efficiency in Asia: An Empirical Analysis. 6th EMAN Selected Papers (Part of EMAN Conference Collection), 49–57. https://doi.org/10.31410/eman.s.p.2022.49

Rosenthal, L. (1983). An empirical test of the efficiency of the ADR market. Journal of Banking & Finance, 7(1), 17–29. https://doi.org/10.1016/0378-4266(83)90053-5

Santana, T., Horta, N., Revez, C., Santos Dias, R. M. T., & Zebende, G. F. (2023). Effects of interdependence and contagion between Oil and metals by ρ DCCA : an case of study about the COVID-19. Sustainability, 15(5), 3945.

Teixeira, N., Dias, R., & Pardal, P. (2022). The gold market as a safe haven when stock markets exhibit pronounced levels of risk : evidence during the China crisis and the COVID-19 pandemic. April, 27–42.

Tran, V. Le, & Leirvik, T. (2020). Efficiency in the markets of crypto-currencies. Finance Research Letters, 35. https://doi.org/10.1016/j.frl.2019.101382

Urquhart, A. (2016). The inefficiency of Bitcoin. Economics Letters, 148, 80–82. https://doi.org/10.1016/J.ECONLET.2016.09.019

Vasco, C., Pardal, P., & Dias, R. T. (2021). Do the stock market indices follow a random walk? Handbook of Research on Financial Management During Economic Downturn and Recovery, 389–410. https://doi.org/10.4018/978-1-7998-6643-5.ch022

Zargar, F. N., & Kumar, D. (2019). Informational inefficiency of Bitcoin: A study based on high-frequency data. Research in International Business and Finance, 47, 344–353. https://doi.org/10.1016/J.RIBAF.2018.08.008

Zebende, G. F., Santos Dias, R. M. T., & de Aguiar, L. C. (2022). Stock market efficiency: An intraday case of study about the G-20 group. Heliyon (Vol. 8, Issue 1). https://doi.org/10.1016/j.heliyon.2022.e08808