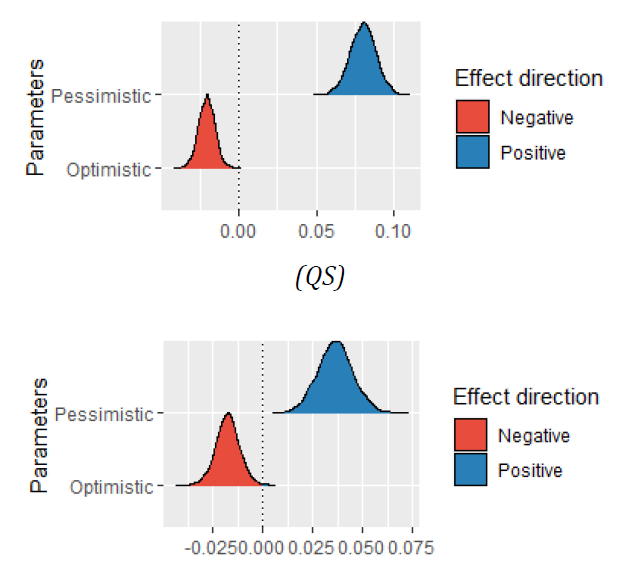

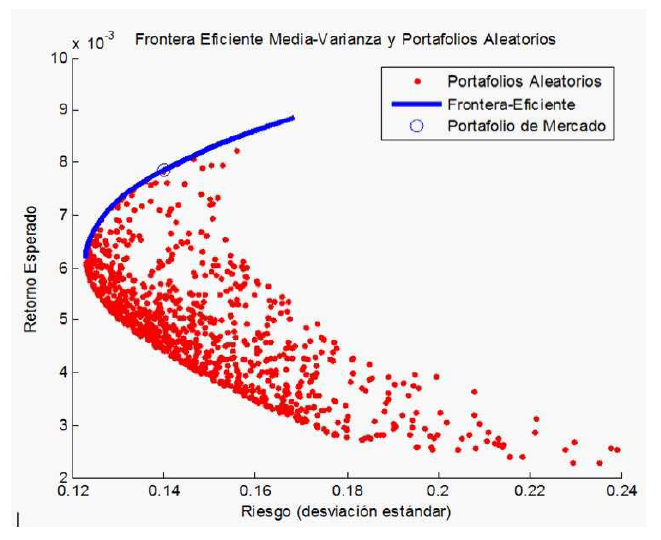

In this paper, a portfolio analysis is carried out using the Sharpe ratio to identify the optimal market portfolio. The measure of investment performance with a Sharpe ratio is compared to results obtained with bootstrapped resamples of the Sharpe ratio. The results indicate that the choice of the market portfolio is highly affected by the uncertainty regarding the estimation of the expected returns and the variance-covariance matrix between the returns, that is, the estimation risk associated with these parameters.

Martinez, R. G. (2023). Portfolio analysis with Sharpe ratios resampled with bootstrapping. Economic Analysis Letters, 2(1), 14. doi:10.58567/eal02010004

ACS Style

Martinez, R. G. Portfolio analysis with Sharpe ratios resampled with bootstrapping. Economic Analysis Letters, 2023, 2, 14. doi:10.58567/eal02010004

AMA Style

Martinez R G. Portfolio analysis with Sharpe ratios resampled with bootstrapping. Economic Analysis Letters; 2023, 2(1):14. doi:10.58567/eal02010004

Chicago/Turabian Style

Martinez, Rolando G. 2023. "Portfolio analysis with Sharpe ratios resampled with bootstrapping" Economic Analysis Letters 2, no.1:14. doi:10.58567/eal02010004

Martinez, R. G. Portfolio analysis with Sharpe ratios resampled with bootstrapping. Economic Analysis Letters, 2023, 2, 14. doi:10.58567/eal02010004

AMA Style

Martinez R G. Portfolio analysis with Sharpe ratios resampled with bootstrapping. Economic Analysis Letters; 2023, 2(1):14. doi:10.58567/eal02010004

Chicago/Turabian Style

Martinez, Rolando G. 2023. "Portfolio analysis with Sharpe ratios resampled with bootstrapping" Economic Analysis Letters 2, no.1:14. doi:10.58567/eal02010004

APA style

Martinez, R. G. (2023). Portfolio analysis with Sharpe ratios resampled with bootstrapping. Economic Analysis Letters, 2(1), 14. doi:10.58567/eal02010004

Article Metrics

Article Access Statistics

References

Auer, B. R., & Schuhmacher, F. (2013). Performance hypothesis testing with the Sharpe ratio: The case of hedge funds. Finance Research Letters, 10(4), 196-208. https://doi.org/10.1016/j.frl.2013.08.001

Bao, Yong, Aman Ullah (2006). Moments of the estimated Sharpe ratio when the observations are not IID, Finance Research Letters, Volume 3, Issue 1, March 2006, pp. 49-56. https://doi.org/10.1016/j.frl.2005.11.001

Boynton, W., & Chen, F. (2018). A parametric bootstrap to evaluate portfolio allocation models. Finance Research Letters, 25, 76-82. https://doi.org/10.1016/j.frl.2017.10.009

Kvam, Paul, Brani Vidakovic (2007), Nonparametric Statistics with Applications to Science and Engineering, Wiley Series in Probability and Statistics, John Wiley & Sons, Inc., Hoboken, New Jersey, pp. 446. DOI: 10.1002/9781119268178

Ledoit, O., & Wolf, M. (2008). Robust performance hypothesis testing with the Sharpe ratio. Journal of Empirical Finance, 15(5), 850-859. https://doi.org/10.1016/j.jempfin.2008.03.002

Morey, M. R., & Vinod, H. D. (2001). A double Sharpe ratio. Advances in Investment Analysis and Portfolio Management, 8, 57-65.

Sharpe, William F. (1964), Capital Asset Prices: A Theory of Market Equilibrium under Conditions of Risk, The Journal of Finance, Vol. 19, No. 3 (Sep. 1964), pp. 425-442. https://doi.org/10.1111/j.1540-6261.1964.tb02865.x

Skrepnek, G. H., & Sahai, A. (2011). An estimation error corrected Sharpe ratio using bootstrap resampling. Journal of Applied Finance and Banking, 1(2), 189.

Vinod, H.D., Morey, M.R. (2001). A double Sharpe ratio. En: Lee, C.F. (Ed.), Advances in Investment Analysis and Portfolio Management, vol. 8. JAI/Elsevier Science, New York, pp. 57-65.