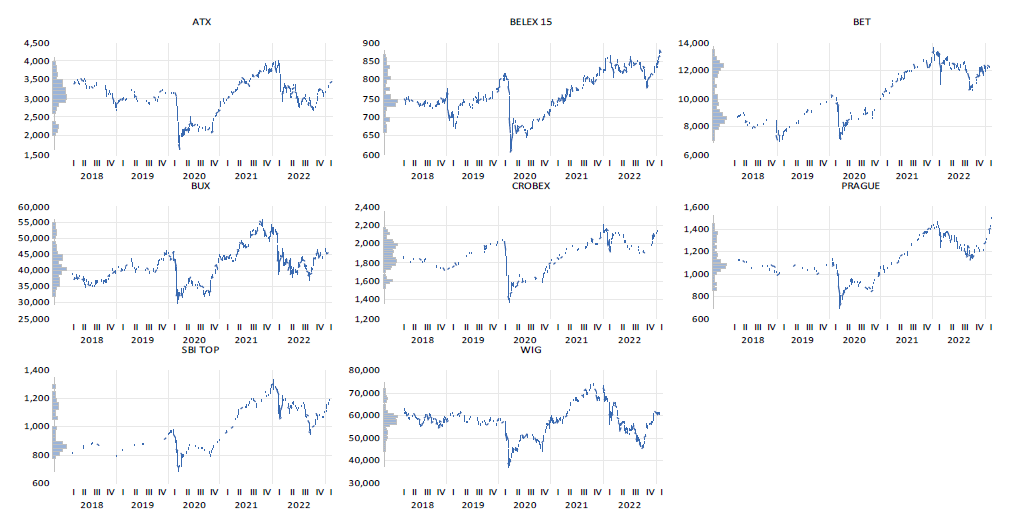

This paper intends to analyze efficiency, in its weak form, in the stock markets of Austria (ATX), Poland (WIG), the Czech Republic (PX Prague), Hungary (BUX), Croatia (CROBEX), Serbia (BELEX 15), Romania (BET), and Slovenia (SBI TOP), from February 16, 2018, to February 15, 2023. To achieve the research aim, we intend to answer the following research question: i) Have events in 2020 and 2022 heightened the persistence of Central European stock markets? Results suggest that persistence in returns has increased significantly during the first wave of Covid-19 and the Russian invasion in the year 2023, but we also saw that most stock markets already exhibit long memories, implying that the research question has been partially validated. This research can provide valuable insights to investors, policymakers, and others interested in financial risk management.

Teixeira Dias, R. M., Chambino, M., & Rebolo Horta, N. (2023). Long-Term Dependencies in Central European Stock Markets: A Crisp-Set Analysis. Economic Analysis Letters, 2(1), 12. doi:10.58567/eal02010002

ACS Style

Teixeira Dias, R. M.; Chambino, M.; Rebolo Horta, N. Long-Term Dependencies in Central European Stock Markets: A Crisp-Set Analysis. Economic Analysis Letters, 2023, 2, 12. doi:10.58567/eal02010002

AMA Style

Teixeira Dias R M, Chambino M, Rebolo Horta N. Long-Term Dependencies in Central European Stock Markets: A Crisp-Set Analysis. Economic Analysis Letters; 2023, 2(1):12. doi:10.58567/eal02010002

Chicago/Turabian Style

Teixeira Dias, Rui M.; Chambino, Mariana; Rebolo Horta, Nicole 2023. "Long-Term Dependencies in Central European Stock Markets: A Crisp-Set Analysis" Economic Analysis Letters 2, no.1:12. doi:10.58567/eal02010002

Teixeira Dias, R. M.; Chambino, M.; Rebolo Horta, N. Long-Term Dependencies in Central European Stock Markets: A Crisp-Set Analysis. Economic Analysis Letters, 2023, 2, 12. doi:10.58567/eal02010002

AMA Style

Teixeira Dias R M, Chambino M, Rebolo Horta N. Long-Term Dependencies in Central European Stock Markets: A Crisp-Set Analysis. Economic Analysis Letters; 2023, 2(1):12. doi:10.58567/eal02010002

Chicago/Turabian Style

Teixeira Dias, Rui M.; Chambino, Mariana; Rebolo Horta, Nicole 2023. "Long-Term Dependencies in Central European Stock Markets: A Crisp-Set Analysis" Economic Analysis Letters 2, no.1:12. doi:10.58567/eal02010002

APA style

Teixeira Dias, R. M., Chambino, M., & Rebolo Horta, N. (2023). Long-Term Dependencies in Central European Stock Markets: A Crisp-Set Analysis. Economic Analysis Letters, 2(1), 12. doi:10.58567/eal02010002

Article Metrics

Article Access Statistics

References

Breitung, J. (2000). The local power of some unit root tests for panel data. Advances in Econometrics, 15. https://doi.org/10.1016/S0731-9053(00)15006-6

Dias, R., Pardal, P., Teixeira, N., & Horta, N. (2022). Tail Risk and Return Predictability for Europe ’ s Capital Markets : An Approach in Periods of the. December. https://doi.org/10.4018/978-1-6684-5666-8.ch015

Dickey, D., & Fuller, W. (1981). Likelihood ratio statistics for autoregressive time series with a unit root. Econometrica, 49(4), 1057–1072. https://doi.org/10.2307/1912517

Fama, E. F. (1965). Random Walks in Stock Market Prices. Financial Analysts Journal, 21(5). https://doi.org/10.2469/faj.v21.n5.55

Fama, E. F. (1970). Efficient Capital Markets: A Review of Theory and Empirical Work. The Journal of Finance, 25(2). https://doi.org/10.2307/2325486

Fama, E. F. (1991). Efficient Capital Markets: II. The Journal of Finance, 46(5). https://doi.org/10.2307/2328565

Fama, E. F., & French, K. R. (1988). Dividend yields and expected stock returns. Journal of Financial Economics, 22(1). https://doi.org/10.1016/0304-405X(88)90020-7

Guedes, E. F., Santos, R. P. C., Figueredo, L. H. R., Da Silva, P. A., Dias, R. M. T. S., & Zebende, G. F. (2022). Efficiency and Long-Range Correlation in G-20 Stock Indexes: A Sliding Windows Approach. Fluctuation and Noise Letters. https://doi.org/10.1142/S021947752250033X

Im, K. S., Pesaran, M. H., & Shin, Y. (2003). Testing for unit roots in heterogeneous panels. Journal of Econometrics. https://doi.org/10.1016/S0304-4076(03)00092-7

Jarque, C. M., & Bera, A. K. (1980). Efficient tests for normality, homoscedasticity and serial independence of regression residuals. Economics Letters, 6(3). https://doi.org/10.1016/0165-1765(80)90024-5

Kantelhardt, J. W., Koscielny-Bunde, E., Rego, H. H. ., Havlin, S., & Bunde, A. (2001). Detecting long-range correlations with detrended fluctuation analysis. Physica A: Statistical Mechanics and Its Applications, 295(3–4), 441–454. https://doi.org/10.1016/S0378-4371(01)00144-3

Levin, A., Lin, C. F., & Chu, C. S. J. (2002). Unit root tests in panel data: Asymptotic and finite-sample properties. Journal of Econometrics, 108(1). https://doi.org/10.1016/S0304-4076(01)00098-7

Pardal, P., Dias, R., Teixeira, N. & Horta, N. (2022). The Effects of Russia ’ s 2022 Invasion of Ukraine on Global Markets : An Analysis of Particular Capital and Foreign Exchange Markets. https://doi.org/10.4018/978-1-6684-5666-8.ch014

Peng, C. K., Buldyrev, S. V., Havlin, S., Simons, M., Stanley, H. E., & Goldberger, A. L. (1994). Mosaic organization of DNA nucleotides. Physical Review E, 49(2), 1685–1689. https://doi.org/10.1103/PhysRevE.49.1685

Phillips, P. C. B., & Perron, P. (1988). Testing for a unit root in time series regression. Biometrika, 75(2), 335–346. https://doi.org/10.1093/biomet/75.2.335

Sun, M., Song, H., & Zhang, C. (2022). The Effects of 2022 Russian Invasion of Ukraine on Global Stock Markets: An Event Study Approach. SSRN Electronic Journal. https://doi.org/10.2139/ssrn.4051987

Teixeira, N., Dias, R., Pardal, P., & Horta, N. (2022). Financial Integration and Comovements Between Capital Markets and Oil Markets : An Approach During the Russian. December. https://doi.org/10.4018/978-1-6684-5666-8.ch013

Zebende, G. F., Santos Dias, R. M. T., & de Aguiar, L. C. (2022). Stock market efficiency: An intraday case of study about the G-20 group. Heliyon 8(1). https://doi.org/10.1016/j.heliyon.2022.e08808