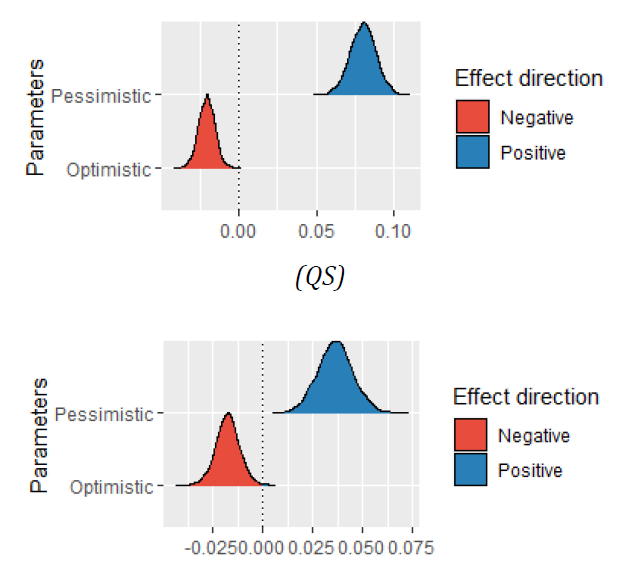

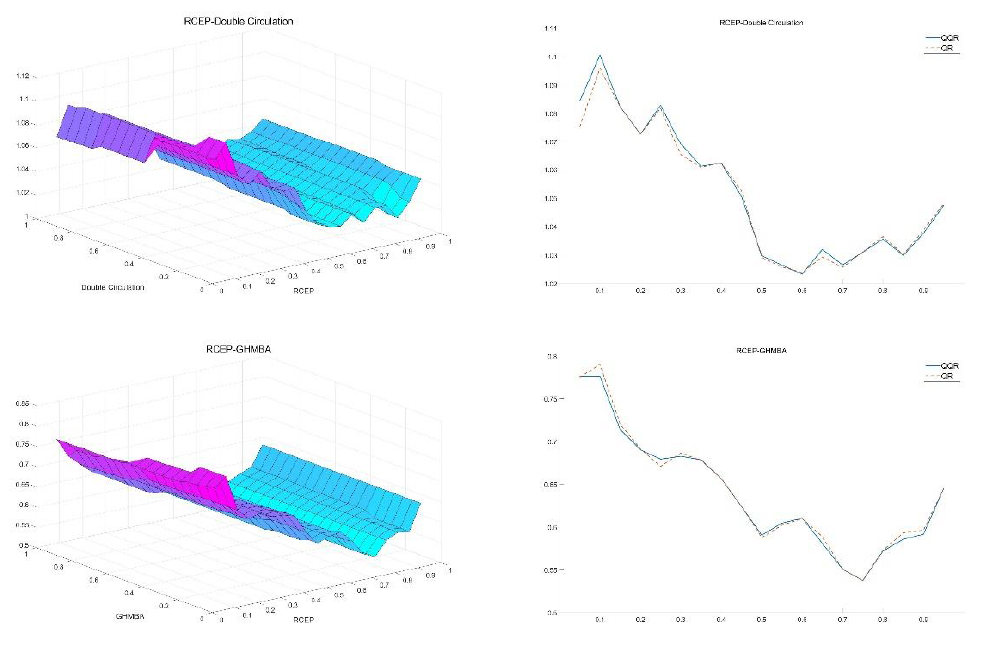

With the daily data from Nov 20, 2019 to Oct 31, 2022, this paper examines the dynamic nonlinear effects of RCEP on Dual Circulation and Greater Bay Area stock market from a quantile perspective. The rolling window quantile regressions detect the positive effects of RCEP on Dual Circulation and Greater Bay Area stock markets with significant time-varying characteristics. Meanwhile, QQ results show that the impacts from RCEP index are more significant under extreme conditions. In addition, we further use a nonparametric QC test to provide evidence on the predictive power of RCEP for Dual Circulation and Greater Bay Area with stock market.

Mo, B., & Nie, H. (2022). The Impact of RCEP on Dual Circulation and Greater Bay Area — From the Perspective of China’s Stock Market Conditions. Economic Analysis Letters, 1(2), 8. doi:10.58567/eal01020003

ACS Style

Mo, B.; Nie, H. The Impact of RCEP on Dual Circulation and Greater Bay Area — From the Perspective of China’s Stock Market Conditions. Economic Analysis Letters, 2022, 1, 8. doi:10.58567/eal01020003

AMA Style

Mo B, Nie H. The Impact of RCEP on Dual Circulation and Greater Bay Area — From the Perspective of China’s Stock Market Conditions. Economic Analysis Letters; 2022, 1(2):8. doi:10.58567/eal01020003

Chicago/Turabian Style

Mo, Bin; Nie, He 2022. "The Impact of RCEP on Dual Circulation and Greater Bay Area — From the Perspective of China’s Stock Market Conditions" Economic Analysis Letters 1, no.2:8. doi:10.58567/eal01020003

Mo, B.; Nie, H. The Impact of RCEP on Dual Circulation and Greater Bay Area — From the Perspective of China’s Stock Market Conditions. Economic Analysis Letters, 2022, 1, 8. doi:10.58567/eal01020003

AMA Style

Mo B, Nie H. The Impact of RCEP on Dual Circulation and Greater Bay Area — From the Perspective of China’s Stock Market Conditions. Economic Analysis Letters; 2022, 1(2):8. doi:10.58567/eal01020003

Chicago/Turabian Style

Mo, Bin; Nie, He 2022. "The Impact of RCEP on Dual Circulation and Greater Bay Area — From the Perspective of China’s Stock Market Conditions" Economic Analysis Letters 1, no.2:8. doi:10.58567/eal01020003

APA style

Mo, B., & Nie, H. (2022). The Impact of RCEP on Dual Circulation and Greater Bay Area — From the Perspective of China’s Stock Market Conditions. Economic Analysis Letters, 1(2), 8. doi:10.58567/eal01020003

Article Metrics

Article Access Statistics

References

Cao, G., & Xie, W. (2022). Asymmetric dynamic spillover effect between cryptocurrency and China's financial market: Evidence from TVP-VAR based connectedness approach. Finance Research Letters, 49, 103070. https://doi.org/10.1016/j.frl.2022.103070

Guo, D., & Zhou, P. (2021). The rise of a new anchor currency in RCEP? A tale of three currencies. Economic Modelling, 104, 105647. https://doi.org/10.1016/j.econmod.2021.105647

Guo, N. (2021). Reasons and Measures for the Development of" Double Circulation" in Post-Epidemic Period in China. Frontiers in Economics and Management, 2(2), 218-224. https://doi.org/10.6981/FEM.202102_2(2).0026

Guo, Q., & Gao, R. (2022). Study on the Present Situation, Problems and Countermeasures of Dual Circulation Development in the Guangdong-Hong Kong-Macao Greater Bay Area. Open Journal of Business and Management, 10(4), 2127-2159. https://doi.org/10.4236/ojbm.2022.104108

Hou, Y., Li, S., & Wen, F. (2019). Time-varying volatility spillover between Chinese fuel oil and stock index futures markets based on a DCC-GARCH model with a semi-nonparametric approach. Energy Economics, 83, 119-143. https://doi.org/10.1016/j.eneco.2019.06.020

Jiang, Y., Jiang, C., Nie, H., & Mo, B. (2019). The time-varying linkages between global oil market and China's commodity sectors: Evidence from DCC-GJR-GARCH analyses. Energy, 166, 577-586. https://doi.org/10.1016/j.energy.2018.10.116

Jiang, Y., Tian, G., & Mo, B. (2020). Spillover and quantile linkage between oil price shocks and stock returns: new evidence from G7 countries. Financial Innovation, 6(1), 1-26. https://doi.org/10.1186/s40854-020-00208-y

Jiang, Y., Tian, G., Wu, Y., & Mo, B. (2022). Impacts of geopolitical risks and economic policy uncertainty on Chinese tourism‐listed company stock. International Journal of Finance & Economics, 27(1), 320-333. https://doi.org/10.1002/ijfe.2155

Li, H., Zhou, D., Hu, J., & Guo, L. (2022). Dynamic linkages among oil price, green bond, carbon market and low-carbon footprint company stock price: Evidence from the TVP-VAR model. Energy Reports, 8, 11249-11258. https://doi.org/10.1016/j.egyr.2022.08.230

Meng, J., Nie, H., Mo, B., & Jiang, Y. (2020). Risk spillover effects from global crude oil market to China’s commodity sectors. Energy, 202, 117208. https://doi.org/10.1016/j.energy.2020.117208

Mo, B., Meng, J., & Zheng, L. (2022). Time and frequency dynamics of connectedness between cryptocurrencies and commodity markets. Resources Policy, 77, 102731. https://doi.org/10.1016/j.resourpol.2022.102731

Nusair, S. A., & Olson, D. (2022). Dynamic relationship between exchange rates and stock prices for the G7 countries: A nonlinear ARDL approach. Journal of International Financial Markets, Institutions and Money, 78, 101541. https://doi.org/10.1016/j.intfin.2022.101541

Qiao, X., Zhu, H., Zhang, Z., & Mao, W. (2022). Time-frequency Transmission Mechanism of EPU, Investor Sentiment and Financial Assets: A Multiscale TVP-VAR Connectedness Analysis. The North American Journal of Economics and Finance, 101843. https://doi.org/10.1016/j.najef.2022.101843

Salem, L. B., Nouira, R., Jeguirim, K., & Rault, C. (2022). The determinants of crude oil prices: Evidence from ARDL and nonlinear ARDL approaches. Resources Policy, 103085. https://doi.org/10.1016/j.resourpol.2022.103085

Sim, N., & Zhou, H. (2015). Oil prices, US stock return, and the dependence between their quantiles. Journal of Banking & Finance, 55, 1-8. https://doi.org/10.1016/j.jbankfin.2015.01.013

Wan, G., Wang, X., Zhang, R., & Zhang, X. (2022). The impact of road infrastructure on economic circulation: Market expansion and input cost saving. Economic Modelling, 112, 105854. https://doi.org/10.1016/j.econmod.2022.105854

Wang, Z., Yu, Z., Ma, L., & Li, A. (2022). The Digital Economy and the Energy “Internal Circulation”: Evidence from China’s Interprovincial Energy Trade. Sustainability, 14(23), 15837. https://doi.org/10.3390/su142315837

Wu, J., & Chen, T. (2022). Impact of Digital Economy on Dual Circulation: An Empirical Analysis in China. Sustainability, 14(21), 14466. https://doi.org/10.3390/su142114466

Yifu, L. J., & Wang, X. (2021). Dual circulation: A new structural economics view of development. Journal of Chinese Economic and Business Studies, 1-20. https://doi.org/10.1080/14765284.2021.1929793

Yousaf, I., & Ali, S. (2020). The COVID-19 outbreak and high frequency information transmission between major cryptocurrencies: Evidence from the VAR-DCC-GARCH approach. Borsa Istanbul Review, 20, S1-S10. https://doi.org/10.1016/j.bir.2020.10.003

Yu, G., & Zhou, X. (2021). The influence and countermeasures of digital economy on cultivating new driving force of high-quality economic development in Henan Province under the background of" double circulation". Annals of Operations Research, 1-22. https://doi.org/10.1007/s10479-021-04325-4

Zhang, C., & Chen, P. (2022). Applying the three-stage SBM-DEA model to evaluate energy efficiency and impact factors in RCEP countries. Energy, 241, 122917. https://doi.org/10.1016/j.energy.2021.122917

Zhang, W., Cao, S., Zhang, X., & Qu, X. (2023). COVID-19 and stock market performance: Evidence from the RCEP countries. International Review of Economics & Finance, 83, 717-735. https://doi.org/10.1016/j.iref.2022.10.013