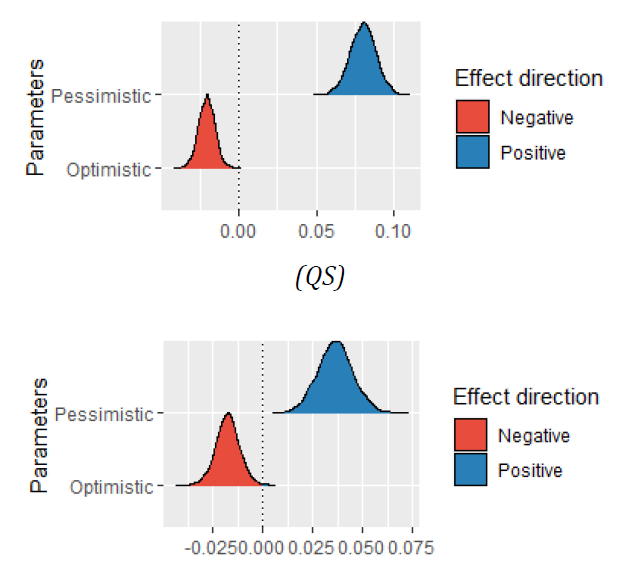

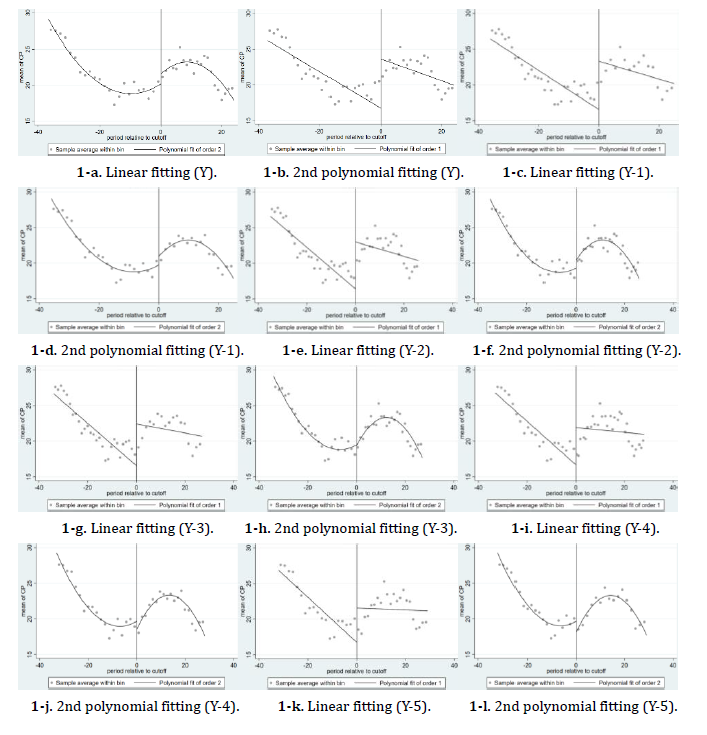

Information leakage in the stock market has been widely proven. Information disclosure is sometimes uneven, and there is significant information asymmetry between ordinary investors and professional institutional investors. In this paper, Regression Discontinuity design (RDD) model is first employed to analyze the information leakage issues. Based on the daily closing stock prices of 15 capital service listed companies, we analyze the difference between the market reaction time and the disclosure time of two stamp tax policies. We found that the sample policies information may leaked to the market about two days earlier. This paper provides a new method analyzing information leakage.

Zhu, J.; Yang, C. Analysis of Stock Market Information Leakage by RDD. Economic Analysis Letters, 2022, 1, 5. doi:10.58567/eal01010005

AMA Style

Zhu J, Yang C. Analysis of Stock Market Information Leakage by RDD. Economic Analysis Letters; 2022, 1(1):5. doi:10.58567/eal01010005

Chicago/Turabian Style

Zhu, Jianing; Yang, Cunyi 2022. "Analysis of Stock Market Information Leakage by RDD" Economic Analysis Letters 1, no.1:5. doi:10.58567/eal01010005

APA style

Zhu, J., & Yang, C. (2022). Analysis of Stock Market Information Leakage by RDD. Economic Analysis Letters, 1(1), 5. doi:10.58567/eal01010005

Article Metrics

Article Access Statistics

References

Aitken, M.J., Aspris, A., Foley, S., and Harris, F.H.D.B. (2018). Market Fairness: The Poor Country Cousin of Market Efficiency. Journal of Business Ethics 147, 5-23, https://doi.org/10.1007/s10551-015-2964-y

Angrist, J.D., and Pischke, J.-S. (2009). Mostly harmless econometrics: An empiricist's companion. Princeton university press.

Calonico, S., Cattaneo, M.D., and Titiunik, R. (2015). Optimal Data-Driven Regression Discontinuity Plots. Journal of the American Statistical Association 110, 1753-1769, https://doi.org/10.1080/01621459.2015.1017578

Cattaneo, M.D., and Titiunik, R. (2022). Regression Discontinuity Designs. Annual Review of Economics 14, 821-851, https://doi.org/10.1146/annurev-economics-051520-021409

Di Maggio, M., Franzoni, F., Kermani, A., and Sommavilla, C. (2019). The relevance of broker networks for information diffusion in the stock market. Journal of Financial Economics 134, 419-446, https://doi.org/10.1016/j.jfineco.2019.04.002

Gelman, A., and Imbens, G. (2019). Why high-order polynomials should not be used in regression discontinuity designs. Journal of Business & Economic Statistics 37, 447-456, https://doi.org/10.1080/07350015.2017.1366909

Kim, T.-Y. (2019). Effect of pre-disclosure information leakage by block traders. Journal of Risk Finance 20, 470-483, https://doi.org/10.1108/jrf-09-2018-0134

Kurov, A., Sancetta, A., Strasser, G., and Wolfe, M.H. (2019). Price Drift Before US Macroeconomic News: Private Information about Public Announcements? Journal of Financial and Quantitative Analysis 54, 449-479, https://doi.org/10.1017/s0022109018000625

Lee, D.S., and Lemieux, T. (2010). Regression Discontinuity Designs in Economics. Journal of Economic Literature 48, https://doi.org/10.1257/jel.48.2.281

Miller, S.R., Li, D., Eden, L., and Hitt, M.A. (2008). Insider trading and the valuation of international strategic alliances in emerging stock markets. Journal of International Business Studies 39, 102-117, https://doi.org/10.1057/palgrave.jibs.8400322